5 Post-Tax Season Financial Wins for Hamilton Business Owners

Finally, April 30 has passed, and that nerve-wracking deadline for tax payments in Canada feels like shedding a heavy backpack after a long hike. For Hamilton business owners, the immediate relief of hitting “submit” on your returns is sweet, but too many let that sigh of relief signal the end of tax thoughts. Here’s the reality: most owners file, celebrate briefly, then ignore finances until next spring, only to face the same scramble amid growing bills and CRA notices.

The real opportunity? Post-tax season is your golden window for proactive Hamilton business owners tax planning. With fresh data from your just-filed returns, you can spot patterns, plug leaks, and set up systems that save thousands come next April. Think better cash flow, fewer surprises, and more money reinvested in your Hamilton hustle. Let’s dive into the five smart moves to make right now.

Why Post-Tax Season Planning Matters for Hamilton Businesses

Tax planning isn’t a seasonal sprint, it’s a year-round marathon that keeps Hamilton businesses ahead of the curve. Many owners treat April 30 like the finish line, but shifting that mindset now unlocks real advantages: smoother cash flow by anticipating outflows, fewer gut-punch surprises from CRA reassessments, and bigger deductions through timely tracking.

In Ontario’s tax landscape, where HST remittance deadlines and provincial credits add layers of complexity, proactive steps are non-negotiable. Hamilton entrepreneurs face unique pressures like CRA’s rigorous audits and local economic shifts businesses that plan post-tax season report up to 20% better savings by nailing compliance early.

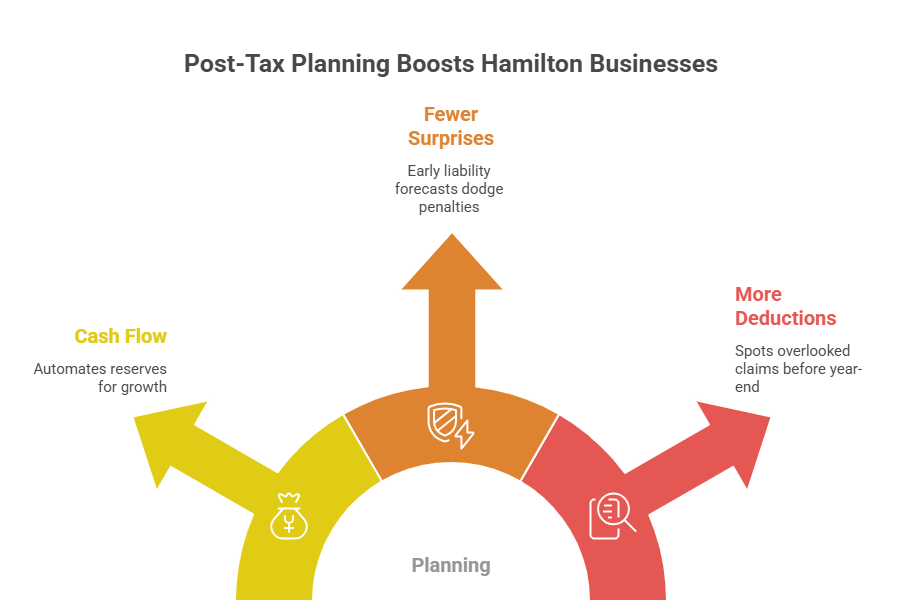

| Benefit | Impact on Hamilton Businesses |

| Cash Flow Management | Automates reserves for quarterly installments, freeing capital for growth |

| Fewer Surprises | Early liability forecasts dodge penalties (up to 10% on late payments) |

| More Deductions | Spots overlooked claims like home office or vehicle expenses before year-end |

Bottom line: Year-round vigilance turns compliance into a competitive edge, especially under Ontario’s rules.

Financial Move #1: Conduct a Mid year financial review (April–June Window)

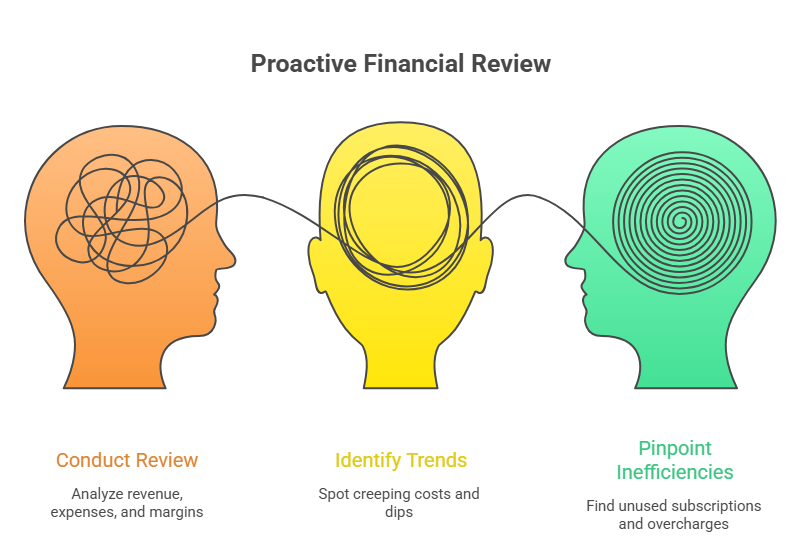

Right after tax season, your first smart move as a Hamilton business owner is to schedule a mid year financial review. Hamilton pros can’t stress enough aim for that sweet April-to-June window while numbers are fresh. Pull your books and dissect revenue against expenses, scrutinize profit margins, and run fresh estimates on tax liabilities. Compare these to last year’s figures to uncover trends, like creeping costs or seasonal dips, and pinpoint inefficiencies such as unused subscriptions or supplier overcharges.

This isn’t busywork; it forecasts taxes early, so you’re not blindsided by installments, and fuels sharper decisions like hiking prices on high-margin services or trimming fat before it balloons.

| Review Focus | Key Metrics to Check | Actionable Outcome |

| Revenue vs. Expenses | Monthly totals YTD | Cut leaks (e.g., 10% overspend flagged) |

| Profit Margins | Gross/net vs. prior year | Adjust pricing for 5-15% gains |

| Tax Liability Estimates | Provisional vs. actual filed | Prep for Q2/Q3 CRA payments |

| Year-over-Year Trends | Growth/decline patterns | Spot inefficiencies early |

Insight: Regular reviews like this slash year-end stress by up to 40% and boost planning accuracy, keeping your Hamilton operation lean and compliant.

Financial Move #2: Set Up a Tax Savings System Immediately

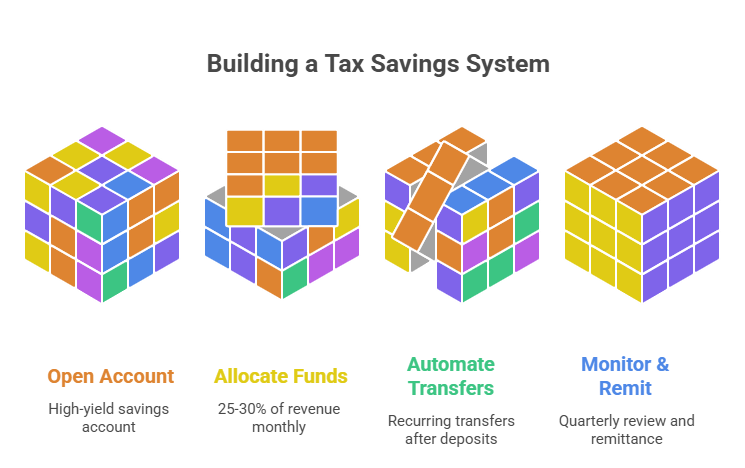

Your second power move? Establish a tax savings account that small business owners in Hamilton rely on to dodge the post-tax crunch. Head to your bank today and open a high-interest separate account dedicated solely to taxes, then commit to allocating 25–30% of gross monthly revenue straight into it, covering income taxes, CPP contributions, and more. Automate those transfers right after deposits hit, so money flows before you can spend it on new gear or that office upgrade.

Don’t forget GST/HST handling: segregate collected remittances here too, remitting them quarterly to stay CRA-compliant and sidestep penalties that start at 1% per month plus interest.

| Step | Action | Pro Tip |

| Open Account | Choose high-yield savings (e.g., 3-4% interest) | Link to business chequing for seamless transfers |

| Allocate Funds | 25-30% of revenue monthly | Adjust based on your effective tax rate from last filing |

| Automate Transfers | Set recurring on the 5th | Include buffer for HST (13% Ontario rate) |

| Monitor & Remit | Review quarterly | Avoids 10% late-filing penalties |

Insight: Automating this system prevents brutal cash flow shocks at tax time, letting Hamilton businesses invest confidently instead of playing catch-up.

Financial Move #3: Optimize Your Tax Strategy for the Rest of the Year

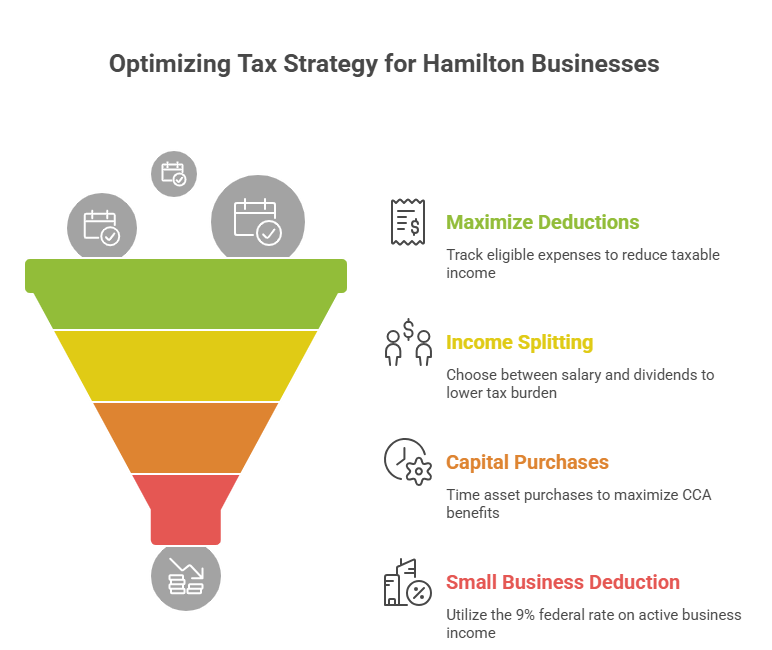

Now we’re getting to the heart of Hamilton business owners tax planning: fine-tuning your approach for the back half of the year to slash your overall bill legally and smartly. Start by maximizing deductions, tracking every eligible expense like home office setups (up to $2 per sq ft or actual costs), vehicle mileage (at CRA-prescribed rates), and supplies that keep your operation humming. Weigh income splitting options too, such as paying family members fair salaries or toggling between salary (for RRSP room) and dividends (often taxed lower for active shareholders).

Strategically time capital purchases for maximum capital cost allowance (CCA), like buying equipment before year-end to claim depreciation right away. Tap into Canada’s Small Business Deduction, which drops the federal rate to 9% on the first $500,000 of active business income for eligible firms.

| Strategy | How It Works | Hamilton Impact |

| Maximize Deductions | Home office, vehicle, supplies | Recoups 20-50% of costs via reduced taxable income |

| Income Splitting | Salary vs. dividends | Lowers family tax bracket creep |

| Capital Purchases | CCA on assets | Accelerates write-offs for cash flow boost |

| SBD Benefit | 9% federal rate on $500K | Saves thousands vs. general 15% rate |

Deductions lower your taxable income directly; tax credits reduce tax owed dollar-for-dollar combine them for firepower.

Insight: This proactive planning cuts your total tax burden by 15-25% while improving cash flow, giving Hamilton owners an edge in a tough market.

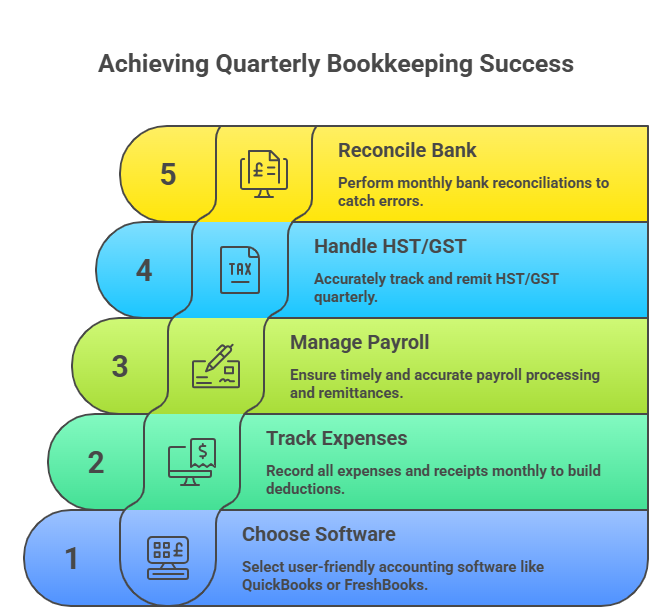

Financial Move #4: Implement Quarterly Bookkeeping & Reporting

Move four in your post-tax playbook: roll out a rock-solid quarterly bookkeeping Hamilton routine to keep your finances humming without the year-end panic. Switch to a monthly or quarterly system using user-friendly accounting software like QuickBooks, FreshBooks, or Wave tools that categorize everything automatically and generate reports with a click. Focus on tracking expenses down to the receipt, payroll obligations, and HST inputs/outputs to ensure you’re remitting accurately every quarter.

This setup matters big time because it banishes last-minute chaos when April rolls around again, and keeps you audit-ready CRA demands records for up to six years, with fines up to $1,000 per violation for slip-ups.

| Tracking Category | Frequency | Why Track It |

| Expenses & Receipts | Monthly | Builds deduction arsenal instantly |

| Payroll | Bi-weekly/monthly | Ensures T4s and remittances are spot-on |

| HST/GST | Quarterly | Matches collections to filings, avoids shortfalls |

| Bank Reconciliations | Monthly | Catches errors before they compound |

Bonus: If your tax owing exceeds $3,000 annually, this preps you perfectly for quarterly installments due June 15, September 15, etc., spreading the load evenly.

Insight: Consistent bookkeeping turns compliance into a breeze, freeing Hamilton business owners to focus on growth over grunt work.

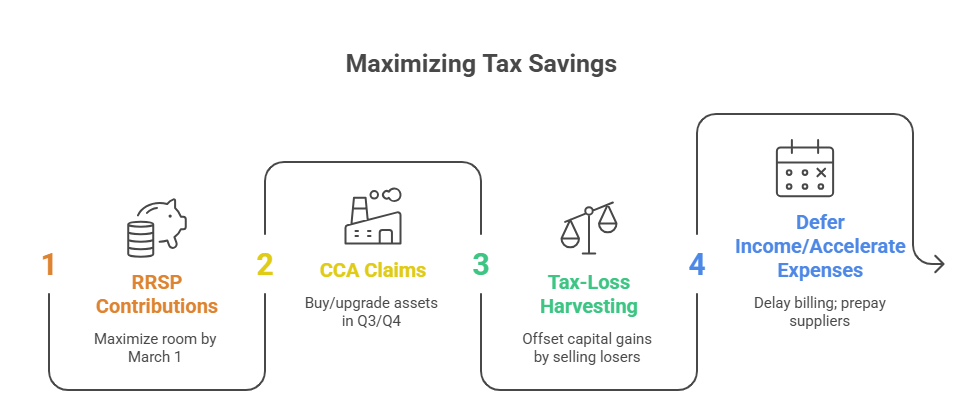

Financial Move #5: Plan Ahead for Tax Savings Opportunities (Before Year-End)

Your fifth and final power play: dive into tax savings strategies Ontario businesses use to front-load year-end wins, starting right now in the post-tax calm. Prioritize RRSP contributions for personal tax relief (deadline March 1 for prior year deductions), claim capital cost allowance (CCA) on depreciable assets like machinery or vehicles to write off costs faster, and if you’ve got investments, practice tax-loss harvesting by selling losers to offset gains. Smart timing seals it’s deferred income to next year (e.g., invoice in January) while accelerating deductible expenses like repairs or marketing before December 31.

These moves compound when planned early, dodging the frantic December rush.

| Strategy | How to Execute | Potential Savings |

| RRSP Contributions | Max your room; contribute by March 1 | Drops taxable income by contribution amount |

| CCA Claims | Buy/upgrade assets Q3/Q4 | 20-100% write-off rates depending on class |

| Tax-Loss Harvesting | Offset capital gains | Up to $3,000 annual carryover |

| Defer Income/Accelerate Expenses | Delay billing; prepay suppliers | Shifts $10K+ to lower brackets |

Insight: Waiting until year-end cramps your options and misses deadlines early planning maximizes savings by 20-30% for Ontario entrepreneurs.

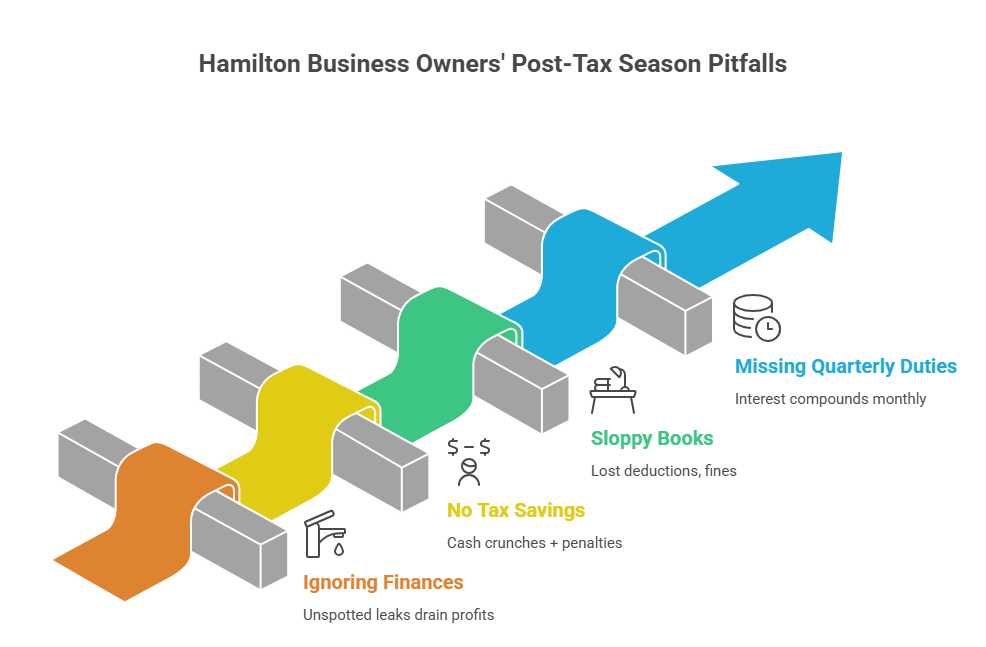

Common Mistakes Hamilton Business Owners Make After Tax Season

After the April 30 high-fives, it’s easy to slip into complacency with business finances after April 30, but these pitfalls trip up even savvy Hamilton owners. First up: ignoring finances entirely until next spring, letting small issues like rising costs snowball into tax nightmares. Second, skipping dedicated tax savings means you’re raiding that pot for “emergencies,” only to face CRA penalties come filing time.

Poor bookkeeping habits rank high, too, stashing receipts in shoeboxes or delaying entries leads to missed deductions and audit flags. And don’t sleep on quarterly obligations: late HST remittances or installment payments trigger interest at prime +2%, eating into your margins fast.

| Mistake | Consequence | Quick Fix |

| Ignoring Finances | Unspotted leaks drain 10-20% profits | Monthly 15-min check-ins |

| No Tax Savings | Cash crunches + 10% penalties | Automate 25-30% reserves now |

| Sloppy Books | Lost deductions, $1K+ fines | Cloud software daily |

| Missing Quarterly Duties | Interest compounds monthly | Calendar reminders + reviews |

Steer clear of these, and business finances after April 30 become your growth accelerator, not a headache.

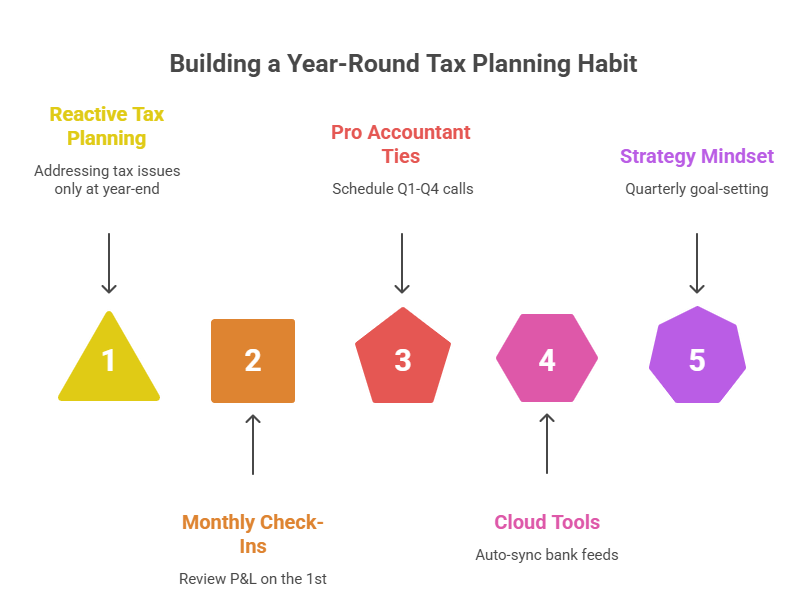

Pro Tips: Build a Year-Round Tax Planning Habit

Lock in lasting success by weaving tax smarts into your daily rhythm. Start with quick monthly financial check-ins, scanning key metrics like cash flow and expenses in just 15-30 minutes. Partner proactively with a Hamilton accountant for quarterly strategy sessions, not just year-end crises, to catch tailored opportunities early.

Embrace cloud accounting tools like QuickBooks Online or Xero for real-time tracking from your phone, anywhere in Hamilton. Above all, reframe taxes as a growth strategy, not a dreaded deadline. This mindset shift uncovers savings year-round.

| Pro Tip | How to Implement | Payoff |

| Monthly Check-Ins | Review P&L on the 1st | Spots issues before they grow |

| Pro Accountant Ties | Schedule Q1-Q4 calls | Custom advice saves 15-25% |

| Cloud Tools | Auto-sync bank feeds | Audit-ready in seconds |

| Strategy Mindset | Quarterly goal-setting | Turns compliance into profit |

Insight: Ongoing planning fuels smarter long-term decisions, helping Hamilton businesses thrive amid CRA rules and economic flux.

FAQ

Q1: What should I do after tax season as a small business owner?

Answer: Jump into a mid year financial review, set up automated tax savings, and start quarterly bookkeeping to build momentum and avoid next year’s rush.

Q2: What are the best financial moves for Hamilton entrepreneurs after April 30?

Answer: The top five: conduct a mid year financial review, open a tax savings account, optimize strategies like CCA and deductions, implement quarterly books, and plan year-end savings early.

Q3: How often should I review my business finances?

Answer: Aim for monthly check-ins and formal quarterly reviews to keep you agile without overwhelming your schedule.

Q4: How can I reduce taxes before year-end in Ontario?

Answer: Leverage RRSP contributions by March 1, accelerate CCA on assets, defer income, and harvest losses; early planning maximizes these under Ontario and CRA rules.

Conclusion: Turn Post-Tax Season Into a Growth Opportunity

April 30 isn’t the finish line for Hamilton business owners tax planning; it’s the starting gun for a smarter financial year ahead. Recap the five moves: launch a mid year financial review, automate your tax savings account, optimize strategies like deductions and CCA, lock in quarterly bookkeeping, and plan year-end savings now.

These steps transform relief into real growth, boosting cash flow and compliance in Ontario’s demanding landscape.

Need help with Hamilton business owners tax planning? Talk to Taxmetic today. Let’s make your 2026 taxes work for you.