Running a business in Ontario means navigating taxes like HST, but many owners trip up on registration timing. Get it wrong, and you face penalties or missed credits. This guide breaks it down simply, based on the latest CRA rules for 2026, so you know exactly when to register for HST and avoid costly mistakes.

Do You Really Need to Register for HST?

Many Ontario business owners register for HST too early, tying up cash in remittances, or too late, racking up CRA fines. The stakes? Penalties up to 5% of uncollected HST plus interest, or lost input tax credits on expenses. Quick preview: If your taxable revenue stays under $30,000 in 12 months, you likely don’t need to register yet. But growth changes everything. For Hamilton business owners, tax planning and timing this right saves thousands.

What Is HST in Ontario?

HST stands for Harmonized Sales Tax, a combo of 5% federal GST and 8% Ontario provincial sales tax, totaling 13% in 2026. You charge it on most goods and services (taxable supplies) sold in Ontario. Exempt supplies like basic groceries or healthcare skip it entirely. Businesses registered for HST collect it from customers, remit it to CRA, and claim credits on their own HST paid purchases. Not everyone must register; it’s revenue driven.

Do You Need to Register for HST in Ontario?

No, you don’t need to register for HST if you’re a small supplier staying under the $30,000 threshold, but yes, mandatory registration kicks in if you exceed it, operate in specific sectors, or choose voluntary registration for tax perks. The Canada Revenue Agency (CRA) bases this strictly on your taxable revenue (gross sales of taxable and zero rated supplies, not profit), measured over any four consecutive calendar quarters. This rolling check gives startups flexibility but demands vigilant tracking.

Think of it like a speed limit: Stay under $30K, cruise freely without “registration.” Hit the threshold, pull over, and register within 29 days or face fines.

Why Revenue, Not Profit?

New business owners often mix this up. A $50K year with $40K expenses (low profit) still triggers if taxable sales top $30K. CRA wants to capture growing sellers who should collect tax on behalf of the government.

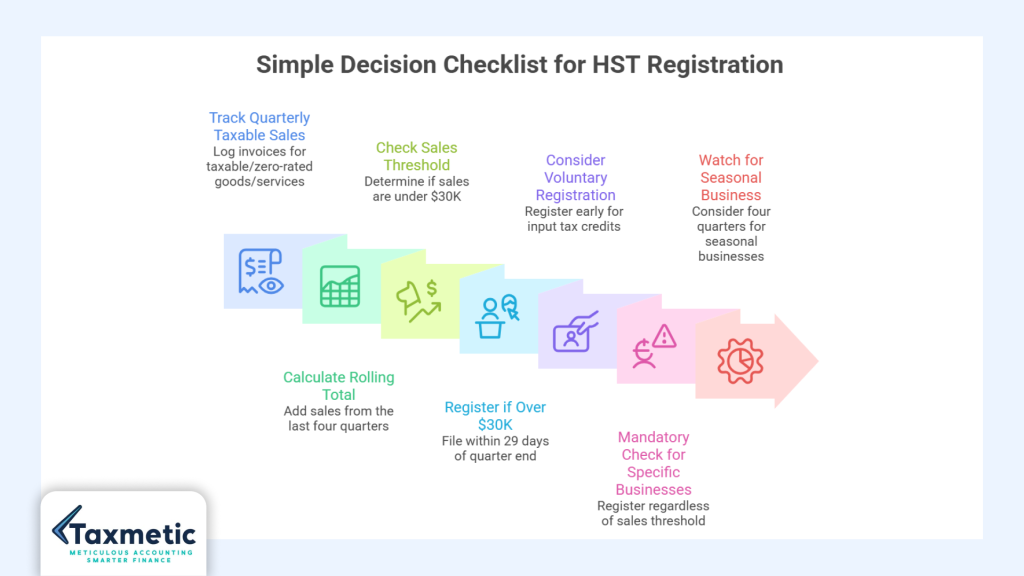

Simple Decision Checklist

Use this step by step to decide today:

- Track Quarterly Taxable Sales: Log every invoice for taxable/zero rated goods/services. Use free tools like QuickBooks or Excel.

- Calculate Rolling Total: Add last four quarters (e.g., Q2, Q5). Under $30K? You’re exempt; no HST collection or filings needed.

- Over $30K? Register Fast: File within 29 days of quarter end. The effective date can be retroactive up to 90 days.

- High Expenses? Go Voluntary: If paying lots of HST on supplies (rent, ads, software), register early for input tax credits (ITCs) and recover up to 13% back.

- Mandatory Check: Rideshares, taxis, or non residents? Register regardless (more in section 9).

- Edge Cases: Seasonal business? One big quarter doesn’t trigger alone; watch the four quarters roll.

| Your Situation | Threshold Status | Next Step |

| Startup: $25K/year | Under $30K | Exempt; monitor growth |

| Freelancer: $35K over 4Q | Over | Register in 29 days |

| E com with $20K sales + $15K expenses | Under but high ITC potential | Consider voluntary |

| Hamilton rideshare driver | Mandatory | Register immediately |

Pro Tip for Hamilton Owners: If you’re scaling a side hustle while filing T1 personal tax returns, this exemption buys time. But pair it with small business tax deductions to maximize savings, many miss ITCs by delaying voluntary registration.

Still unsure? Run your numbers with a tax accountant in Hamilton. One quick consult prevents thousands in penalties.

The $30,000 Small Supplier Rule Explained.

This is the core rule for “HST registration threshold Ontario”. CRA’s small supplier exemption keeps paperwork light for startups.

What Is a Small Supplier?

Under CRA rules, you’re a small supplier if your worldwide taxable revenues (including zero rated supplies) are $30,000 or less in the last four consecutive calendar quarters. Nonprofits and public bodies have a $50,000 limit. Publicly traded shares or financial services don’t count toward this.

The 4 Consecutive Calendar Quarters Rule

CRA looks at Q1 Q4 rolling: Jan Mar, Apr Jun, etc. Add your taxable sales from the latest four. Exceed $30K? You’re out of small supplier status.

Exceeding $30,000 in One Quarter vs Multiple Quarters

Hit $30K+ in one quarter? Register immediately if projecting over annually. But the rule triggers on the four quarter total, giving breathing room for seasonal spikes.

Real Life Examples

- Freelancer Scenario: Graphic designer earns $8K/quarter. Total: $32K over four quarters. Must register by the end of the fifth quarter.

- Small Business Growth: Hamilton café hits $35K in Q3 alone but averages $25K prior. Tracks four quarter roll: registers when total crosses $30K.

| Scenario | Q1 | Q2 | Q3 | Q4 | 4 Quarter Total | Action |

| Steady Freelancer | $7K | $8K | $8K | $9K | $32K | Register |

| Seasonal Retail | $5K | $10K | $20K | $5K | $40K | Register |

| Under Threshold | $6K | $6K | $7K | $6K | $25K | Exempt |

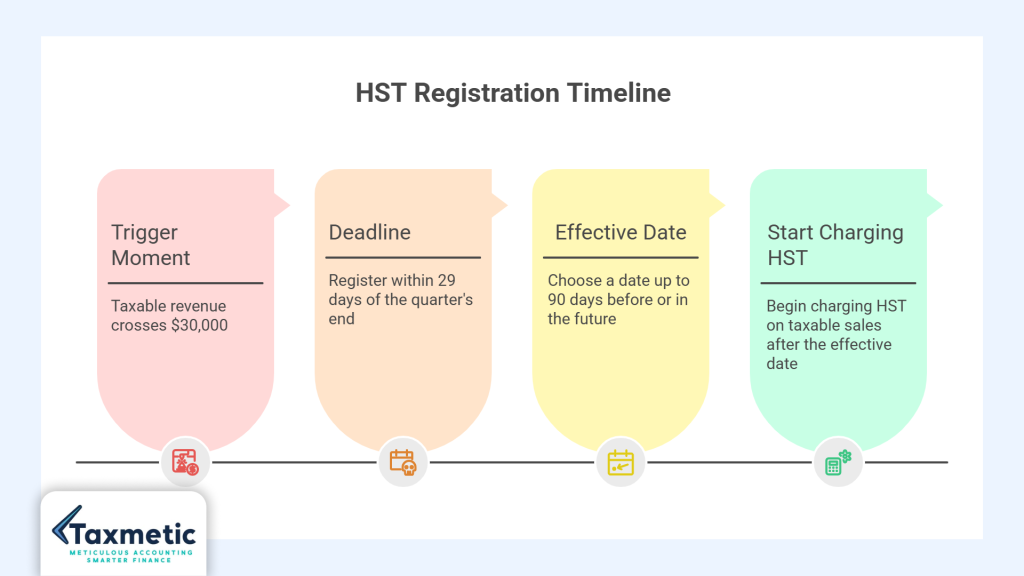

When Exactly Do You Have to Register for HST?

The clock starts ticking the moment your taxable revenue crosses $30,000 over any four consecutive calendar quarters. You must register within 29 days of that trigger quarter’s end, no extensions. For instance, if Q3 (Jul Sep) pushes your Q1 Q3 + Q4 projection over, register by October 28.

Key Timelines Breakdown

- Trigger Moment: End of the quarter where four quarter total ≥ $30K.

- Deadline: 29 days later (e.g., Sep 30 trigger to Oct 29 deadline).

- Effective Date: Your choice can be up to 90 days before registration (retroactive for ITC claims) or in the future. But you cannot collect HST before this date.

- Start Charging HST: On all taxable sales after the effective date. Update invoices immediately.

Timeline Example: Freelancer Crosses $30K

| Quarter | Revenue | Notes |

| Q1 (Jan Mar) | $7,000 | |

| Q2 (Apr Jun) | $8,000 | |

| Q3 (Jul Sep) | $9,000 | Register by Oct 29. Effective: Oct 1 (retroactive OK)Charge HST on Oct+ sales |

| Q4 (Oct Dec) | $8,000 | Register by Oct 29Effective: Oct 1 (retroactive OK)Charge HST on Oct+ sales |

What If You Miss the 29 Day Window?

CRA can force registration retroactively, making you liable for uncollected HST out of pocket. Penalties: 5% of the owed amount + 1% monthly interest (compounded daily). Real case: Ontario retailer delayed by 2 months owed $12K HST + $1,800 fines.

Action Steps Post Trigger

- Log in to CRA My Business Account.

- Select HST (RT0001) account.

- Note the effective date carefully, and consult a pro to maximize ITCs.

- Notify clients; update POS/invoicing.

For growing Hamilton businesses, sync this with quarterly reviews to avoid surprises.

What Revenue Counts Toward the HST Threshold?

Included:

- Taxable supplies (e.g., consulting fees, product sales).

- Zero rated supplies (e.g., exports, basic groceries, 0% HST but count toward threshold).

Not Included:

- Exempt supplies (e.g., rent, healthcare).

- Personal income, grants, or loans.

| Supply Type | HST Rate | Counts Toward $30K? |

| Taxable (e.g., marketing services) | 13% | Yes |

| Zero Rated (e.g., exports) | 0% | Yes |

| Exempt (e.g., education) | N/A | No |

Do You Need to Register for HST Under $30,000?

Short answer: No, if strictly under. But if expecting growth or with big HST expenses (office supplies, software), voluntary registration lets you claim input tax credits (ITCs). Common myth: “Profit under $30K means exempt.” No, it’s gross taxable revenue.

Voluntary HST Registration in Canada: Is It Worth It?

Yes, if expenses exceed HST collected, recover ITCs on purchases. Pros: Cash back, looks pro to clients. Cons: Quarterly filings, admin burden. Ideal for e-commerce or service pros in small business tax deductions, like Hamilton owners chasing every credit.

Pros vs Cons Table:

| Pros | Cons |

| Claim ITCs on expenses | Must file returns (even if zero) |

| Boosts credibility | Collect/remit on all sales |

| Retroactive option | Potential audits |

Who Must Register for HST Regardless of Income?

- Ride sharing/taxi services (mandatory since 2017).

- Air/boat carriers.

- Non residents selling into Canada.

Check CRA’s full list of revenue threshold doesn’t apply here.

HST Exempt vs Taxable Services in Ontario

Exempt (No HST charged or collected):

- Healthcare, education, and child care.

- Most financial services, residential rent.

Taxable:

- Consulting, marketing, e-commerce.

- Professional services like tax accountants in Hamilton.

This affects your threshold; exempt sales don’t count, delaying registration.

How to Register for HST in Ontario (Step by Step)

Targeting “how to register for HST CRA” searches? Here’s the 2026 process.

- Get a Business Number (BN): Sole props use existing SIN; others apply via CRA’s Business Registration Online (BRO).

- Register Online: Use CRA’s My Business Account. Select HST account (RT0001).

- Receive HST number Ontario: Instant or 10 15 days; format like 123456789RT0001.

- Start Charging: Add 13% to invoices post-effective date. File returns quarterly/annually.

What Happens If You Register Late?

Delaying HST registration beyond the 29 day deadline isn’t just paperwork; it’s expensive. CRA enforces strict rules: You become liable for all HST you should have collected retroactively, paid out of pocket (no chasing old customers). Penalties stack fast, wiping profits.

CRA Penalties Breakdown (2026 Rules)

- Failure to Register Penalty: 5% of HST you should have collected/remitted from the effective date.

- Interest: 1% per month (compounded daily) on unpaid amounts, from the due date.

- Gross Negligence Penalty: Up to 25% if deemed intentional (rare but severe).

- No Grace Period: CRA can assess back 3 4 years via audit.

Quick Penalty Example: $10K HST owed on late sales.

- 5% penalty: $500.

- 3 months interest (at 1%/month): ~$300.

- Total hit: $10,800+ (and rising).

| Owed HST | 5% Penalty | 1 Month Interest | 3 Months Interest | Total After 3 Mo. |

| $5,000 | $250 | $50 | $155 | $5,405 |

| $10,000 | $500 | $100 | $310 | $10,910 |

| $15,000 | $750 | $150 | $465 | $16,365 |

| $20,000 | $1,000 | $200 | $620 | $21,820 |

Real World Scenarios

- Toronto Retailer (2025 Case): Delayed 60 days on $15K sales. Paid $15K HST + $2,500 penalty + $900 interest = $18,400 total. “Wiped our holiday profits,” per owner.

- Hamilton Freelancer: Crossed threshold Jan 2026, registered April. Owed $8K + $1,200 penalties, could’ve claimed ITCs if timely.

- E com Seller: Seasonal spike ignored; CRA audit added $25K back taxes. Lesson: Track rolling quarters monthly.

How to Avoid It

- Monthly Revenue Reviews: Use apps like Wave or QuickBooks to set $7.5K/quarter alerts.

- Pro Help: Tax accountants in Hamilton like Taxmetic monitor for you.

- Voluntary Early: Register ahead if close to the threshold to avoid the rush.

Bottom line: One late month costs more than a year’s accounting fees. For small business owners, prevention beats cure.

Common HST Registration Mistakes to Avoid

- Tracking profit instead of revenue.

- Ignoring four quarter roll up.

- Missing zero rated supplies in totals.

- Registering early without ITC needs to tie up cash.

For T1 personal tax return filers moonlighting in businesses, double check.

Frequently Asked Questions:

Q: Do I need to register for HST if I earn under $30,000?

Answer: No, as a small supplier, but voluntary if ITCs help.

Q: When should I register for HST in Ontario?

Answer: Within 29 days of exceeding $30K over four quarters.

Q: How to register for HST with CRA?

Answer: Online via BRO; get BN first.

Q: What is an HST number Ontario?

Answer: 9 digit BN + RT0001 (e.g., 123456789RT0001).

Q: Can I register voluntarily for HST in Canada?

Answer: Yes, for ITCs if expenses are high.

Final Thoughts: Should You Register for HST Now?

Recap: Stay under $30K? Exempt. Growing or expense heavy? Register for credits. Use our checklist to track revenue monthly. For Hamilton small business owners, pair with smart tax planning.

Ready to Handle HST Compliance?

Don’t guess, Taxmetic’s Ontario experts make HST registration seamless, from BN setup to filings. Book a free consult today and focus on growth, not CRA headaches.