Why Your T1 Tax Return Matters More Than You Think

Filing your T1 Personal Tax Return is not just a yearly chore; it’s a critical step in managing your financial health in Canada. Every resident with even a fraction of income, a new job, or life‑changing events like marriage or buying a home must file a T1 Income Tax and Benefit Return with the Canada Revenue Agency (CRA).

Why every Canadian must file a T1 personal tax return

Even if your employer already deducted tax from your pay, the CRA still needs your T1 personal tax return to reconcile what you were supposed to owe, what you actually paid, and what benefits you qualify for. A filed T1 return is also the gateway to programs like the Canada Child Benefit (CCB), GST/HST credit, provincial child benefits, and income‑based housing or tuition subsidies.

If you missed a year or didn’t file despite owing tax or benefit repayments, you may face interest charges, late‑filing penalties, and delays in receiving future benefits. For many Canadians, simply landing a new job, starting side‑income work, or earning capital gains from a sold asset triggers the obligation to file, even if you think “I don’t make enough to worry about taxes.”

The real impact of filing correctly

Filing your T1 tax return accurately can directly affect how much money you get back or how much you owe. A careful return can turn missed deductions and forgotten credits into hundreds or even thousands of dollars more in refunds.

Beyond cash, accurate filing helps you:

- Confirm eligibility for benefits and credits based on your actual income.

- Keep your records clean ahead of an audit or CRA review.

- Avoid surprise instalment bills or reassessments later.

Common problems people face when filing taxes

Many Canadians rush through their T1 personal tax return and end up with avoidable issues such as:

- Missing income slips (T4, T5, T2202, etc.) or side income like Gig work, rental income, or crypto‑related gains.

- Under‑claiming deductions like RRSP contributions, childcare expenses, or moving‑related costs.

- Wrong personal information, either outdated addresses or incorrect marital status and dependant details, can delay refunds or benefits.

- Last‑minute filing stress, which leads to rushed CRA profiles, missing NETFILE‑eligible documents, or even missing the April 30 deadline altogether.

What this guide will help you achieve (clarity + checklist + savings)

This 2026 T1 Personal Tax Return checklist is designed to take you from confusion to confidence. You’ll get:

- Clear, plain‑language explanations of what a T1 Income Tax and Benefit Return really is and who must file.

- A step‑by‑step checklist covering all major income types: employment, investments, rental, and self‑employment.

- Practical guidance on deductions and credits you may be missing, plus how life events like marriage, children, or home buying change your tax situation.

By the end, you’ll have a single, organized list you can use every year, while positioning Taxmetic.ca as the smart choice if you’d rather have a professional handle your T1 filing and maximize your refund.

What Is a T1 Personal Tax Return in Canada?

A T1 Personal Tax Return, officially called the T1 Income Tax and Benefit Return, is the main form every Canadian resident uses to report their income, claim deductions and credits, and calculate how much tax they owe (or how much they’ll get back) in a given tax year. Think of it as your annual “tax report card” that the Canada Revenue Agency (CRA) uses to determine your federal and provincial taxes, plus your eligibility for key benefits and credits.

Definition of T1 Income Tax and Benefit Return

The T1 Income Tax and Benefit Return is not just about “paying taxes.” It’s a comprehensive document that:

- Records all types of income (employment, self‑employment, investments, rental, and various benefits).

- Lets you subtract eligible deductions (like RRSP contributions or childcare expenses) to reduce your taxable income.

- Allows you to apply tax credits (medical, tuition, disability, donations) that can cut your final tax bill or boost your refund.

The form also links to several schedules and benefit applications, so one T1 return can unlock things like the Canada Child Benefit (CCB), GST/HST credit, and several provincial income‑based programs.

Who needs to file a T1 personal tax return?

You may need to file a T1 personal tax return even if you don’t think you “owe tax.” Common situations include:

- Employees who received T4 slips or similar income documents.

- Freelancers, gig‑economy workers, and self‑employed individuals who earn income from side hustle work, consulting, or selling services.

- Business owners with corporations or sole‑proprietorships, even if they didn’t take a big salary.

- Investors who earn interest, dividends, or capital gains from stocks, mutual funds, crypto, or real estate.

- Part‑time, low‑income, or new residents who want to receive benefits like CCB or GST/HST credit.

The CRA clearly states that you must file a return if you owe tax, need to repay a benefit, dispose of capital property, or simply want to receive certain benefits.

What information does a T1 tax return include

A typical T1 personal tax return groups data into four main buckets:

| Category | What it covers |

| Income | Employment (T4), self‑employment, rental, investment (T5, T3), pensions, etc. |

| Deductions | CCB, GST/HST credit, and provincial benefits tied to your T1 filing. |

| Tax credits | Medical expenses, donations, tuition, disability, and other personal credits. |

| Benefits & programs | CCB, GST/HST credit, provincial benefits tied to your T1 filing. |

When you file, the CRA uses this information to calculate your refund or balance owing and to confirm whether you qualify for any income‑based benefits that depend on your “net family income” as reported on the T1.

Difference between T1 and Notice of Assessment

Many people confuse the T1 tax return with the Notice of Assessment (NOA). In simple terms:

- The T1 Personal Tax Return is what you file with the CRA each year.

- The Notice of Assessment is what the CRA sends back after processing your return, confirming your assessed income, tax, and any balances or refunds.

The NOA also shows details like your RRSP deduction limit, carried‑forward credits (tuition, loss carry‑forwards), and any outstanding balances or instalments. Keeping your NOA from the last few years is a smart habit, especially when preparing your 2026 T1 personal tax return, because it helps you avoid repeating mistakes and track how your financial picture changes over time.

T1 Tax Return 2026: Important Deadlines You Must Know

The 2026 tax‑filing season for your T1 Personal Tax Return is not something you can push to the last minute. Missing key dates can trigger penalties, interest charges, and delays in your refund or benefit payments. Knowing the exact T1 tax return 2026 deadlines helps you stay compliant while giving you more control over your money.

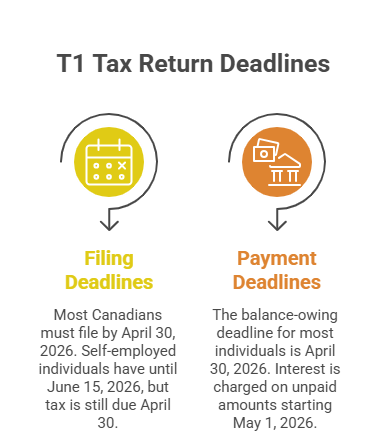

Filing deadlines: April 30 vs June 15 for self‑employed

For most Canadians, the T1 filing deadline for the 2025 tax year is April 30, 2026. This is when your completed T1 Income Tax and Benefit Return must be filed with the CRA, either online or by mail.

If you (or your spouse/common‑law partner) are self‑employed, you get a bit more breathing room for filing your deadline is June 15, 2026. However, this extension only applies to filing the return; any tax you owe is still due by April 30, 2026.

So, if you’re a freelancer, gig‑worker, contractor, or small‑business owner, plan:

- Use June 15 to clean up your self‑employment records and business‑expense details.

- Pay by April 30 to avoid interest on your balance owing.

Payment deadlines and interest on unpaid tax

Filing is one thing; paying is another. The balance‑owing deadline for most individuals is April 30, 2026, regardless of whether you’re employed or self‑employed.

If you don’t pay everything by this date:

- The CRA starts charging interest on the unpaid amount, starting May 1, 2026.

- For repeated late payments, the CRA may require instalment payments in 2027 to avoid future interest.

You can choose from several payment methods (online banking, credit card via third‑party processors, pre‑authorized debit, cash at participating financial institutions), but timing matters: some methods take a few business days to process, so it’s safer to pay a few days before April 30.

Late‑filing penalties explained

Filing your T1 personal tax return late can cost you more than just peace of mind. The CRA applies two main types of penalties:

- Late‑filing penalty

- If you owe tax and file after April 30, 2026, the CRA charges 5% of the balance owing plus 1% per full month for up to 12 months, with a maximum of 12 months.

- If you’ve been late in any of the previous three years, the penalty can be doubled, up to 10% of the balance owing plus 2% per month.

- Interest on unpaid tax

- Even if you only file a day late, interest runs on any unpaid tax from May 1, 2026, onward.

These penalties are designed to encourage on‑time filing and payment, so aligning your schedule with the T1 tax return 2026 deadlines is one of the easiest ways to avoid extra costs.

Why filing early can increase your refund

Filing early isn’t just about avoiding penalties; it can actually put money in your pocket sooner and sometimes even help you claim more. Here’s how:

- Faster refunds and benefit payments

Many people file their T1 personal tax return in March or early April mainly because it shortens the wait for their refund and any benefit adjustments (like CCB, GST/HST, or provincial credits). - More time to catch errors

If you discover missing slips or forget a deduction (like an RRSP contribution or medical expense), you can correct your return before the deadline instead of rushing at the last minute. - Better planning for 2026

When you see your Notice of Assessment early, you understand your RRSP room, outstanding instalments, and any extra tax owing. This helps you set a realistic budget and avoid surprises later in the year.

By treating your T1 Income Tax and Benefit Return like a financial planning tool, not just a CRA form, you can turn a mandatory task into a proactive step toward higher refunds and better compliance.

Complete T1 Personal Tax Return Checklist (2026)

Filing your T1 Personal Tax Return for the 2025 tax year becomes much smoother when you tackle it in categories. This 2026 T1 tax return checklist is designed to help employees, freelancers, investors, and small‑business owners gather everything in one place before they start their return.

Below, each subsection aligns with common CRA expectations and accounting‑firm checklists, so nothing important slips through the cracks.

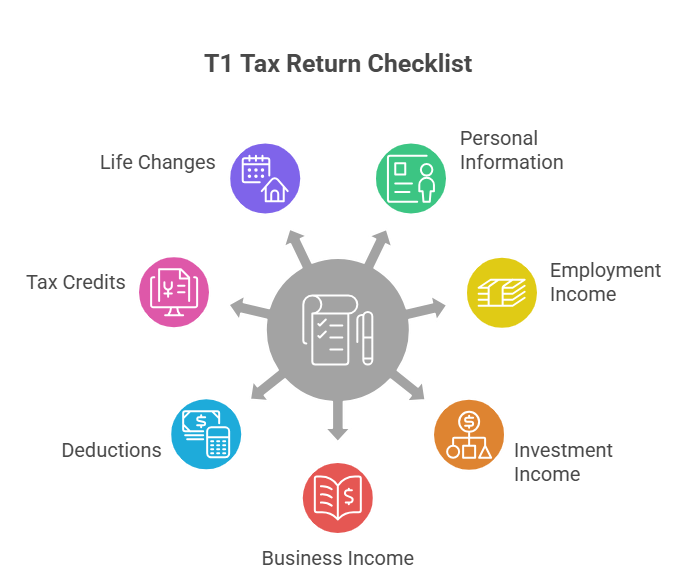

1. Personal Information & CRA Details

Before you jump into income and deductions, your personal details must be correct. Any mistakes here can delay refunds, cause reassessments, or even trigger address‑based benefit issues.

Make sure you have:

- SIN number: Double‑check your Social Insurance Number on your tax software or NETFILE profile, especially if you’re filing for the first time or after a legal name change.

- Updated address & contact details: Notify the CRA of any changes to your home address, e‑mail, or phone number, so you receive your Notice of Assessment, T4As, and any benefit letters on time.

- Marital status: Indicate your status as of December 31, 2025: single, married, common‑law, or separated. This affects combined-income benefits (like CCB), spousal credits, and some deductions.

- Dependents’ information: Collect details for each child or dependant (full name, date of birth, SIN, relationship), plus any amounts they earned in 2025. This is crucial for claiming the Canada Child Benefit, child‑care deductions, and other dependent-related credits.

Keeping a small “life‑event log” in your phone or calendar (marriage, separation, new child, move, or business changes) makes updating your T1 personal tax return faster every April.

2. Employment Income Documents

Most Canadians start their T1 Income Tax and Benefit Return with employment slips. If you’re missing even one, your CRA assessment may be incomplete or delayed.

Gather:

- T4 slips (employment income)

These show your employment income, employment‑insurance premiums, CPP contributions, and any taxable benefits. Include all T4s from every job you held in 2025.

- T4A (freelance / pension income)

Use T4A slips for:- Pension or annuity payments

- Certain self‑employment or contract work

- Scholarship or bursary income

- EI sickness or other supplemental benefits that aren’t T4E.

- T4E (employment insurance)

If you received Employment Insurance (EI) in 2025 (regular, sickness, caregiving, or parental benefits), the T4E shows your EI earnings and any tax withheld.

Also, grab any unslip income (tips, commissions, cash side‑jobs, or gig‑economy work) and keep transaction records or app summaries for 2025.

3. Investment & Rental Income Records

If you earned interest, dividends, or capital gains, or rented out property, you need organized records for your T1 tax return for 2026.

Slips and statements

- T5 (interest income)

From banks, credit unions, or investment firms, T5s show interest income and any tax withheld. - T3 (dividends/trust income)

These slips report dividends, capital gains distributions, and other trust‑related income from mutual funds, ETFs, or trusts. - Capital gains (stocks, crypto, property)

For every stock sale, mutual‑fund distribution, crypto trade, or real estate transaction in 2025, keep:- Purchase price and date

- Sale price and date

- Transaction fees

- Any adjustments for splits or reorganizations.

- Only 50% of capital gains are taxable, while 50% of capital losses can offset gains or carry forward.

Rental income and expenses

If you rented out a property (entire home, basement, or room) in 2025, the CRA expects you to report net rental income or loss.

Prepare a simple summary like this (you can expand it for each rental property):

| Category | Example items to track (2025) |

| Rental income | Monthly rent, security deposits (if kept as income), parking or pet fees. |

| Expenses | Mortgage interest (not principal), property taxes, insurance, repairs, utilities, condo fees, advertising, and management fees. |

| Depreciation | Capital cost allowance (CCA) on appliances or renovations (used carefully, since it can trigger recapture on sale). |

You’ll usually summarize this on Form T776 or within your tax software, but clear records help you defend your numbers if the CRA ever asks.

4. Self‑Employment & Business Income

Self‑employed individuals and small‑business owners often miss key details on their T1 personal tax return, which can trigger reassessments or audits.

Profit & loss statements

- Pull your 2025 income statement (or profit‑and‑loss report) from your accounting software or spreadsheets.

- The CRA uses this to fill out Form T2125 (Statement of Business or Professional Activities), which separates business income from personal employment income.

Business expenses

You can deduct most reasonable expenses that are directly related to earning your self‑employment income, including:

- Office supplies, marketing, website fees, software subscriptions

- Professional services (legal, accounting)

- Travel, mileage, and home‑office costs (if applicable)

- Equipment, tools, and some purchases over a certain threshold (depreciated via CCA).

Keep receipts, bank statements, and card summaries that prove these expenses.

GST/HST collected & paid

If your business is GST/HST‑registered, your T1 return may still need data that ties into your GST/HST filings, such as:

- GST/HST you collected on sales

- GST/HST you paid on business inputs (often claimed as input tax credits).

Keeping your GST/HST returns handy during T1 prep helps you avoid double‑counting or misclassifying income.

Home office expenses

If you worked from home in 2025, you may be able to claim home‑office expenses:

- A portion of rent, utilities, and maintenance is based on square footage or the number of rooms used for work.

The CRA has specific rules for home‑office claims, so ensure your calculation method is consistent and documented.

5. Deductions You Should Not Miss

Deductions reduce your taxable income, which often leads to a bigger refund or lower tax bill. Yet many Canadians overlook simple ones.

Here are key deductions to review for your T1 personal tax return:

- RRSP contributions: Contributions made in the first 60 days of 2026 (up to March 2, 2026) can still count toward your 2025 tax year. Keep contribution receipts and confirm your remaining RRSP room with your prior NOA.

- Childcare expenses: You can deduct eligible childcare costs (licensed daycare, certain babysitters, summer camps) if they allow you or your spouse to work or study.

- Union or professional dues: Fees paid to professional associations, unions, or licensing bodies may be deductible if they’re required for your job.

- Moving expenses: If you moved for work or school (certain distance and condition thresholds apply), you may deduct transportation, storage, and some travel costs.

- Student loan interest: Interest paid on qualifying government student loans in 2025 is deductible, even if you’re no longer in school.

To help you scan, here’s a compact table of common deductions:

| Deduction category | Typical 2025 documentation |

| RRSP contributions | RRSP contribution slips, bank or broker statements. |

| Childcare expenses | Receipts from daycare, camp, or childcare providers. |

| Union/professional dues | Membership invoices or association statements. |

| Moving expenses | Bills for movers, travel, storage, and new‑home setup. |

| Student loan interest | Loan statements showing interest paid in 2025. |

6. Tax Credits That Increase Your Refund

Tax credits directly reduce the amount of tax you owe and can sometimes create a refund even if you don’t owe any tax.

Common credits that often boost a T1 personal tax return include:

- Medical expenses: You can claim eligible medical expenses for yourself, your spouse/common‑law partner, and dependants once total expenses exceed a set percentage of your net income (usually around 3% for 2025).

- Charitable donations: Donations to qualified Canadian charities can generate federal and provincial credits. The first $200 generates a smaller credit, while amounts over $200 create a higher‑rate credit, making larger donations more valuable.

- Tuition credits: If you’re a student or have unused credits from prior years, you can apply them to your 2025 tax or transfer them to certain family members.

- Disability tax credit (DTC): If you or a dependant is eligible for the DTC, you can claim a federal non‑refundable credit and possibly a provincial one, plus open doors to other disability‑related benefits.

Because some credits are non‑refundable and others create refundable components, pairing them with your deduction strategy can significantly improve your refund outcome.

7. Life Changes That Impact Your Taxes

Major life events in 2025 can reshape your T1 personal tax return for 2026. Ignoring these changes can mean leaving credits on the table or accidentally over‑claiming something.

Common life‑event changes to watch:

- Marriage or separation: Marital status affects combined‑income benefits like CCB, some non‑refundable credits, and spousal deduction options.

- Having children: New children can unlock child‑benefit payments, disability‑related credits (if applicable), and increased child‑care expense claims.

- Buying or selling a home: A home purchase may let you claim the Home Buyers’ Amount or coordinate with the Home Buyers’ Plan (HBP).

Selling a home that isn’t your principal residence can trigger capital gains or losses that must be reported. - Moving provinces: If you moved between provinces in 2025, your provincial tax brackets and credits change, and you may need to file with more than one jurisdiction.

- Starting or closing a business: Launching a business means you now have self‑employment income and more deductions to track. Closing a business may create capital gains, losses, or decommissioning expenses that must be reported on your T1.

Tracking these life‑event changes in a simple yearly log makes your T1 personal tax return not only accurate but also a powerful tool for maximizing savings and benefit eligibility.

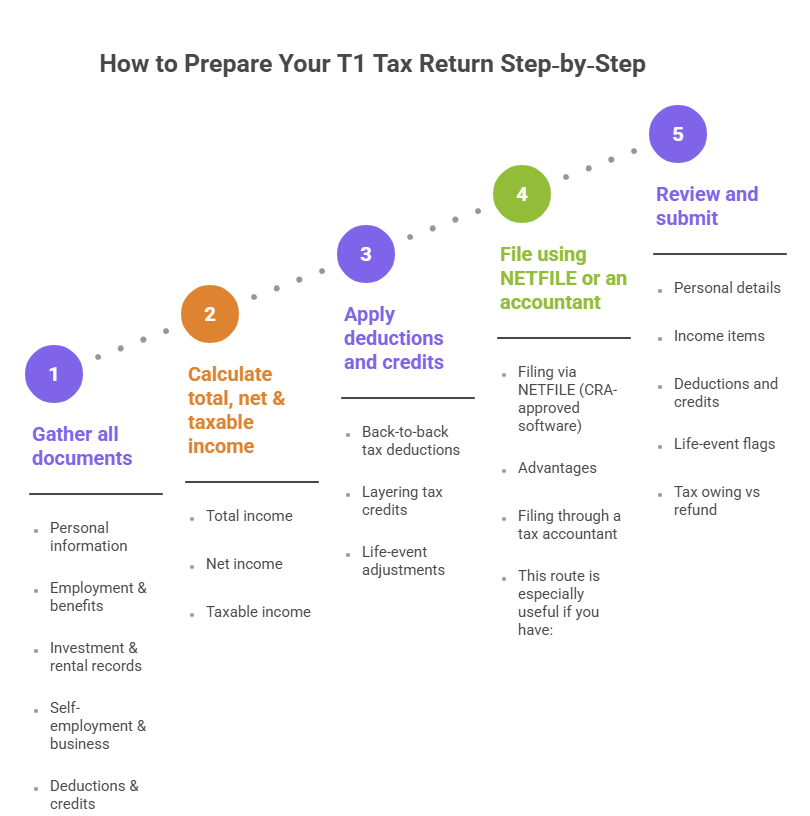

How to Prepare Your T1 Tax Return Step‑by‑Step

Filing your T1 Personal Tax Return becomes less stressful when you break it into a clear five‑step process. This approach works whether you’re using tax software, a cloud‑based accountant, or preparing your own T1 Income Tax and Benefit Return before handing it to a professional.

Each step below aligns with your 2026 checklist, so you can move from messy paperwork to a clean, CRA‑ready return.

Step 1: Gather all documents

Before you open tax software or send anything to an accountant, collect everything in one place. Think of this as your T1 tax return prep kit for 2026.

At a minimum, you should have:

- Personal information

- SIN number

- Current address and contact details

- Marital status as of December 31, 2025

- Dependents’ details (names, dates of birth, SINs)

- Employment & benefits

- All T4 slips (employment income)

- T4A slips (pension, annuity, certain self‑employment, EI‑related payments)

- T4E (Employment Insurance)

- Any other income documents (tips, contract work, gig‑economy summaries)

- Investment & rental records

- T5 (interest), T3 (dividends and trust income)

- Capital gains/loss statements (stocks, crypto, property)

- Rental‑income and expense records (or T776‑style summaries)

- Self‑employment & business

- Profit‑and‑loss statements or T2125 data

- Invoices, receipts, and bank statements for business expenses

- Home‑office and vehicle‑use logs (if applicable)

- Deductions & credits

- RRSP contribution receipts (including those made in early 2026 for 2025)

- Childcare, union/professional dues, moving expenses, and student‑loan‑interest receipts

- Medical‑expense receipts, donation receipts, tuition or education‑related forms (T2202A/TL11A), and DTC paperwork if applicable

Organizing these in folders (physical or digital) saves time and reduces the chance of missing something important when you actually start your T1 personal tax return.

Step 2: Calculate total, net & taxable income

Once your documents are together, the next step is to build your income picture. Most tax software now does this automatically, but understanding the logic helps you spot mistakes.

- Total income

Add up all sources:- Employment income (T4)

- Self‑employment income (T2125)

- Investment income (T5, T3, T5013, etc.)

- Rental income

- Government benefits and other taxable amounts

This is your gross income before any deductions.

- Net income

From total income, subtract certain deductions the CRA allows at this stage, such as:- RRSP contributions

- Certain employment‑related expenses

- Some support‑payment amounts

The result is your net income, which determines your access to many credits and benefits.

- Taxable income

From net income, you subtract additional deductions like:- Childcare expenses

- Moving expenses

- Certain business‑related amounts

The final number is your taxable income, which is used to calculate your federal and provincial tax.

If you’re using tax software, it walks you through these steps behind the scenes. If you’re working with an accountant, they’ll usually ask you to provide numbers or spreadsheets so they can double‑check your calculations.

Step 3: Apply deductions and credits

After you know your taxable income, the next phase is to reduce your tax bill with deductions and credits. This is where many Canadians leave money on the table.

Key actions include:

- Back‑to‑back tax deductions

- Ensure all eligible deductions (RRSP, childcare, moving, student‑loan interest, etc.) are entered at the right stages.

- Check that your RRSP deduction limit (from a prior Notice of Assessment) is respected so you don’t accidentally over‑claim and create a future reassessment.

- Layering tax credits

- Federal and provincial non‑refundable credits (basic personal, age, spouse, dependant, tuition, medical, disability, etc.) are applied to your tax.

- Refundable credits (parts of GST/HST credit, some provincial credits) can create a refund even if you don’t owe tax.

- Life‑event adjustments

- Update marital status, dependants, home‑purchase details, or business‑status changes so your T1 personal tax return reflects 2025 reality.

This step is where a professional can often spot extra savings, especially if you have self‑employment, rentals, investments, or unusual life events, but it’s still vital to review it yourself, even if you go through an accountant.

Step 4: File using NETFILE or an accountant

Once your income, deductions, and credits are in place, you’re ready to file. You have two main paths: self‑filing via NETFILE or using a tax professional.

- Filing via NETFILE (CRA‑approved software)

- Choose a NETFILE‑eligible program that matches your complexity (simple employment vs self‑employment or investments).

- Enter your information, then click NETFILE to send your T1 Income Tax and Benefit Return directly to the CRA.

- Advantages:

- Fast processing (often within two weeks).

- Instant confirmation that the CRA received your return.

- Lower cost than hiring an accountant for simple returns.

- Filing through a tax accountant

- Forward your organized documents and interview notes to your accountant.

- They prepare your T1 personal tax return, optimize deductions and credits, and file it on your behalf (often via certified software or EFILE).

- This route is especially useful if you have:

- Self‑employment or multiple‑business income

- Rental properties or complex investments

- Foreign‑income or foreign‑asset reporting

- Unusual deductions or credits (DTC, HBP, FHSA, etc.)

Many people use a hybrid approach: they gather all documents themselves, then have a professional review or file for them.

Step 5: Review and submit

Before you hit submit, take a few minutes to review everything. This final check is critical for avoiding reassessments, refund delays, or missed savings.

Your quick review checklist should include:

- Personal details

- SIN, address, date of birth, marital status, and dependant details all match reality.

- Income items

- All T4, T4A, T4E, T5, T3, and rental‑income entries are present.

- No obvious omissions (side income, one‑time payments, or crypto transactions).

- Deductions and credits

- RRSP contributions, childcare, moving, and student‑loan‑interest claims are accurate.

- Medical expenses and donation totals are consistent with your receipts.

- Life‑event flags

- Marriage, separation, new child, home purchase, or business change details are up to date.

- Tax owing vs refund

- Check the balance owing or refund amount and ensure it makes sense given your income and deductions. If it seems unusually high or low, recheck key entries.

Once you’re comfortable, submit. If you filed online, you’ll usually receive a confirmation screen and, later, a Notice of Assessment showing your official tax, refund, or balance owing.

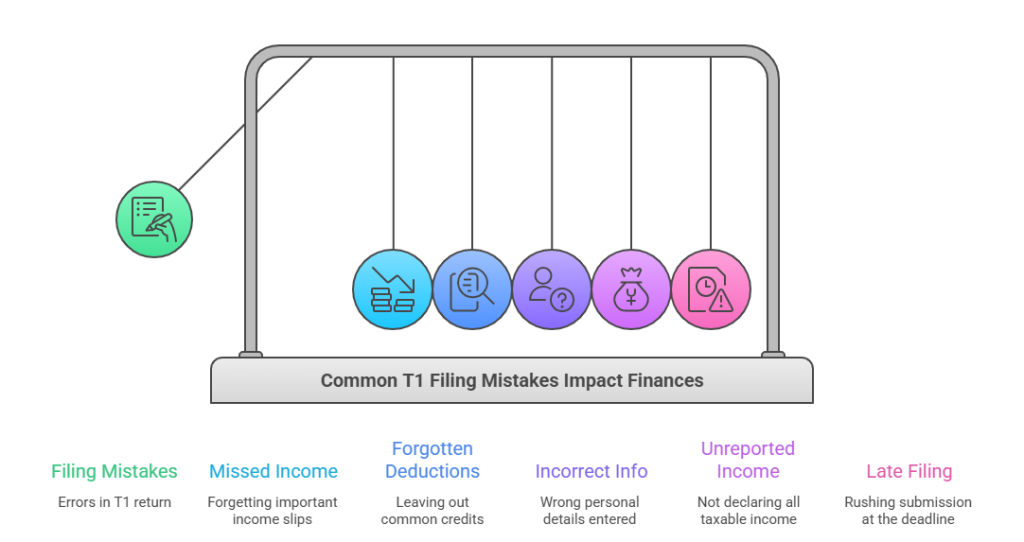

Common Mistakes to Avoid When Filing T1 in 2026

Filing your T1 Personal Tax Return correctly can mean the difference between a smooth refund and a surprise notice from the CRA. Even small errors can trigger reassessments, interest, or delayed benefits.

Below are the most frequent mistakes Canadians make in 2026 and how to avoid them so your T1 Income Tax and Benefit Return stays accurate and stress‑free.

1. Missing income slips

Many taxpayers rush to file without checking their “My Account” or collector e‑mails, which can leave important slips out of their T1 tax return.

Typical omissions include:

- Forgetting a T4 from a short‑term job, seasonal work, or a second employer.

- Not including T4A, T4E, T5, or T3 slips for pensions, EI, interest, dividends, or distributions.

- Overlooking T2202A or TL11A for tuition credits, assuming they’re “not needed this year.”

To avoid this:

- Log in to CRA My Account and download or confirm all slips for 2025.

- Match each slip type (T4, T4A, T5, etc.) against your tax‑software list before you file.

2. Forgetting deductions or credits

Leaving out common deductions and credits is one of the easiest ways to reduce your refund or increase your tax owing.

Frequently forgotten items:

- RRSP contributions made in early 2026 for the 2025 tax year. Many people delay buying until March, but don’t upload the receipt to their software.

- Childcare expenses and eligible employment‑related expenses (home office, union dues, professional fees).

- Medical expenses and charitable donations, especially when spread across multiple providers or charities.

- Tuition and education credits are carried forward or transferred to a spouse or parent.

To catch these:

- Do a checklist pass using the CRA‑style “common deductions and credits” list or your previous year’s NOA to see what you claimed.

- Ask yourself: “What did I pay for in 2025?” for categories like RRSP, childcare, donations, and medical.

3. Incorrect personal information

Wrong personal details are surprisingly common and can delay refunds, cause benefit errors, or trigger identity checking messages from the CRA.

Key mistakes:

- Using an outdated address so benefit cheques or correspondence are mailed to an old home.

- Entering the wrong SIN or a spouse’s SIN by mistake, especially when filing returns for both partners.

- Forgetting to update marital status after a marriage, separation, or common‑law formation, which affects combined‑income benefits and credits.

- Listing dependants incorrectly (wrong dates of birth, adding a child who no longer qualifies, or omitting a newborn).

To avoid this:

- Double‑check your SIN, date of birth, address, marital status, and dependants’ details before you proceed to step 3 in your tax software.

- If you moved in 2025, confirm that you’ve also updated your address with the CRA via My Account.

4. Not reporting side income

With apps, gig platforms, and side‑hustle income, many Canadians assume small amounts “don’t need to be reported.” In reality, all taxable income must appear on your T1 personal tax return, regardless of slip status.

Common under‑reported sources:

- Rideshare, delivery apps, freelancing, drop‑shipping, or selling goods online without a T4A.

- Rental income from a basement, room, or short‑term vacation rental that’s not professionally tracked.

- Crypto or NFT trades that generate capital gains but weren’t properly recorded.

- Cash‑paid work (contracting, web design, cleaning, tutoring, etc.) without invoices or records.

To stay compliant:

- Treat your T1 Income Tax and Benefit Return as a full‑income report, not just a slip‑collector.

- Keep a simple log of 2025 side‑income (date, platform, amount, service type) and estimate it if you don’t have exact figures.

5. Filing late or rushing submission

Many Canadians wait until the last week of April, then file in a hurry, often leading to errors they could have caught if they’d started earlier.

Risks of last‑minute filing:

- Late‑filing penalties if you owe tax and file after April 30, 2026 (or after June 15 if you’re self‑employed but still owe by April 30).

- Interest on any unpaid tax from May 1, 2026, even if you only file a day late.

- Missing simple deductions or credits because you’re skimming forms instead of reviewing them carefully.

Tips to avoid rushing:

- Start gathering documents in January–February and aim to file by mid‑to‑late March.

- If you’re using an accountant, book your appointment early so they have time to review and optimize your T1 tax return for 2026.

- If you know you’ll file late, at least estimate your balance owing and pay it by April 30 to avoid extra interest and larger penalties.

By watching for these common mistakes, missing slips, forgotten deductions, wrong personal info, unreported side income, and last‑minute filing, you can turn your T1 Personal Tax Return from a source of stress into a clean, accurate snapshot of your 2025 finances.

Should You File Yourself or Hire a Tax Accountant?

Deciding whether to file your T1 Personal Tax Return on your own or hand it to a professional is one of the most practical choices you’ll make each tax season. With the right guidance, you can save money if your situation is simple, and avoid costly mistakes when it’s more complex.

DIY vs professional comparison

Here’s a quick comparison between doing it yourself and hiring a tax accountant, tailored to your T1 tax return 2026 context:

| Factor | DIY (self‑filing) | Hiring a tax accountant |

| Cost | Lower upfront cost (software only, or free CRA‑approved options). | Higher fee, but can often pay for itself in extra deductions and credits. |

| Control | Full control over every field and number entry. | You provide documents; accountant handles preparation and optimization. |

| Speed | Fast if you’re organized and your return is simple. | May take days to weeks, depending on the accountant’s workload. |

| Error risk | Higher if you’re unfamiliar with deductions, credits, or complex rules. | Lower, especially for rentals, self‑employment, or investments. |

| Compliance confidence | Good for straightforward returns (single job, minimal deductions). | Strong for complex situations (multiple income sources, foreign assets, etc.). |

If your T1 Income Tax and Benefit Return is mostly employment‑based and you’re comfortable with online tools, DIY may be the right fit. If you have multiple moving pieces or feel unsure, a professional often pays off both in peace of mind and in your final refund.

When DIY works

Filing your own T1 personal tax return is a smart, cost‑effective option when:

- You have one main employer and receive mostly T4 income, with no self‑employment or rental activity.

- Your deductions and credits are straightforward: basic RRSP contributions, standard personal credits, and maybe a few charitable donations.

- You’re comfortable using CRA‑approved tax software (NETFILE) and double‑checking your entries before submission.

If this sounds like you, DIY filing can be quick, cheap, and perfectly compliant as long as you follow a solid checklist like the one in this guide.

When you NEED a professional

There are several scenarios where handing your T1 tax return 2026 to an accountant or firm like Taxmetic becomes almost essential, not just helpful.

Multiple income sources

If you juggle:

- Employment income plus freelance or gig‑economy earnings

- Investment income from stocks, mutual funds, or crypto

- Rental income from one or more properties

Then your tax return stops being “simple.”

An accountant can:

- Properly separate income types

- Track capital gains vs capital losses

- Ensure you don’t double‑count or miss deductions across sources

Self‑employment

If you’re self‑employed, your T1 Income Tax and Benefit Return often includes:

- Form T2125 (Statement of Business or Professional Activities)

- Complex business‑expense tracking

- Home‑office, vehicle, and other indirect deductions

- Potential GST/HST linkages

Trying to DIY all of this without experience can lead to missed deductions, incorrect expense calculations, or audit‑triggering inconsistencies. A professional helps you maximize write‑offs while staying within CRA rules.

Rental or investments

Owning rental properties or managing a diversified investment portfolio introduces layers of complexity:

- Rental income and expenses (repairs, utilities, depreciation) must be clearly separated from personal costs.

- Capital gains and losses from stock, crypto, or real estate sales, where 50% of gains are taxable.

Mistakes here can create unintentional tax bills or missed refund opportunities. An accountant will review your records, ensure correct reporting, and help you plan for future years.

Making it a conversion bridge

For many Canadians, the real choice isn’t just “me vs accountant,” but “how much time and risk am I willing to accept?”

- DIY makes sense when your life is simple, your income is predictable, and you’re confident in your numbers.

- Hiring a professional makes sense when:

- You have multiple income sources, such as self‑employment, rentals, or investments

- You want to maximize every deduction and credit

- You’d rather stay 100% CRA‑compliant and focus on your career, business, or family instead of tax math

This is where Taxmetic can step in: we handle your T1 Personal Tax Return so you don’t miss a single dollar, while you keep your time free for what matters most.

Frequently Asked Questions:

Q: What is a T1 personal tax return?

Answer: A T1 personal tax return is the main form Canadians use to report their income, deductions, and credits to the Canada Revenue Agency (CRA) for a given tax year. It’s also officially called the T1 Income Tax and Benefit Return, because it determines how much tax you owe or your refund and whether you qualify for benefits like GST/HST credit, Canada Child Benefit, and certain provincial programs.

Q: What documents are required for a T1 tax return?

Answer: To prepare your T1 tax return for 2026, you generally need:

- Personal information: SIN, address, marital status, dependants’ details.

- Income slips: T4 (employment), T4A (pension, freelance, EI‑related), T4E (Employment Insurance), T5 (interest), T3 (dividends), plus rental or investment‑related statements.

- Deduction and credit receipts: RRSP contribution slips, childcare, medical expenses, charitable donations, tuition forms, and any other proof of eligible deductions or credits.

Having these documents organized in one place makes your T1 personal tax return faster, cleaner, and less likely to attract a reassessment.

Q: When is the T1 filing deadline for 2026?

For the 2025 tax year, the T1 filing deadline for 2026 is:

- April 30, 2026, for most taxpayers.

- June 15, 2026, for self‑employed individuals and their spouses/common‑law partners (but any tax owed is still due by April 30).

Missing these deadlines can trigger late‑filing penalties and interest, so it’s smart to aim to file earlier in the season.

Q: Can I file my T1 tax return myself?

Answer: Yes, you can file your T1 personal tax return yourself using CRA‑approved tax software that supports NETFILE. This route works well if your income is simple (mainly one job, no rentals, minimal investments) and you’re comfortable double‑checking your entries.

However, hiring a professional tax accountant significantly reduces the risk of errors and often helps you claim more deductions and credits than you would on your own, especially if you have self‑employment, multiple income sources, rentals, or investments.

Conclusion: Filing Your T1 Tax Return the Right Way in 2026

Filing your T1 Personal Tax Return doesn’t have to be stressful. With the right checklist and a bit of preparation, you can turn tax season into a quick, organized process that actually helps you keep more money.

Having a clear plan prevents small mistakes like missed slips or forgotten credits from eating away at your refund. When you file your T1 Income Tax and Benefit Return early and accurately, you gain better control over your finances and stay fully CRA‑compliant.

Ready to File Your T1 Return Without Stress?

If the idea of juggling slips, checking deductions, and staying CRA‑compliant in 2026 still feels heavy, you don’t need to do it alone. At Taxmetic, our goal is to take the pressure off while ensuring you:

- Avoid costly mistakes like missed income, wrong personal info, or under‑reported deductions.

- Maximize every deduction and credit tied to your T1 Income Tax and Benefit Return, from RRSPs and childcare to medical expenses and tuition.

- Stay 100% CRA compliant, even if you have self‑employment, rentals, or complex investments.

Let Taxmetic handle your T1 personal tax return so you don’t miss a single dollar.

Book your consultation today, and we’ll walk you through a smooth, stress‑free 2026 filing experience.