Salary vs Dividends in Canada: How Should Hamilton Business Owners Pay Themselves?

As a Hamilton business owner in 2026, deciding how to pay yourself a salary vs dividends Canada 2026 style can make or break your tax bill, retirement savings, and peace of mind. One wrong move, and you’re handing thousands to the CRA while skimping on your future. The quick answer? It depends, but most owners use a mix of both for optimal results. This guide breaks it down with Ontario specific insights, tax comparisons, real scenarios, and strategies tailored for Hamilton entrepreneurs like you. We’ll cover tax implications, RRSP perks, CPP contributions, and when to blend salary and dividends.

Salary vs Dividends in Canada (Quick Overview)

Salary is like a regular paycheck: your corporation pays you as an employee, deducting it as a business expense before corporate taxes hit. Dividends, on the other hand, come from after tax corporate profits, flexible payouts without payroll hassle.

The key difference? Salary lowers your T2 corporate tax vs personal tax equation by being deductible, while dividends are taxed personally with credits to smooth things out.

Here’s a quick comparison table for clarity:

| Factor | Salary | Dividends |

| Corporate Deduction | Yes (reduces T2 tax) | No (from after tax profits) |

| CPP Contributions | Yes (employee + employer) | No |

| RRSP Room | Yes (18% of earned income) | No |

| Tax Credits | Standard personal rates | Dividend tax credit (gross up) |

| Flexibility | Fixed payroll schedule | Anytime from profits |

Supporting insight: Salary shrinks your corporation’s taxable income, but dividends offer tax credits that often balance the scales through “integration.”

How Salary Works for Business Owners in Ontario

For Hamilton pros searching “owner manager salary Hamilton,” salary means treating yourself as an employee, complete with payroll source deductions.

Tax Treatment of Salary

Your corporation deducts salary as an expense, slashing its taxable income. You then pay personal marginal tax rates on it (federal + Ontario combined, up to 53.53% at top brackets in 2026). It’s straightforward but immediate.

CPP Contributions Explained (2026)

In 2026, CPP maxes at about $7,668 total per person (employee share ~$3,834 + employer match). As owner manager, your corp pays both sides, doubling the hit but building retirement security. Why care? CPP provides a steady income later, unlike dividends.

RRSP Contribution Benefits

Salary shines here: Earned income creates RRSP room up to 18% (max ~$33,540 in 2026). Defer taxes and grow wealth tax free, perfect for long term planning in Hamilton business owners tax planning.

Pros and Cons of Salary

Pros:

- Generates RRSP room for tax deferred growth

- Builds CPP for retirement

- Counts fully for mortgages/credit

Cons:

- Payroll admin and remittances

- Higher upfront personal tax + CPP costs

How Dividends Work in Canada

Searching “dividend vs salary Ontario” or “pay yourself corporation Canada”? Dividends let you distribute profits without the salary rigmarole.

What Are Dividends?

These are shareholder payouts from after tax corporate earnings, not deductible, so your T2 pays first.

Eligible vs Non Eligible Dividends (Very Important Section)

In Hamilton (“eligible dividends Hamilton”) and across Ontario (“non eligible dividends Ontario”), it hinges on your corp’s income type.

- Eligible Dividends: From general business income taxed at higher corporate rates (~26.5% Ontario small business outside limit). Get a 38% gross up with ~15 20% federal credit, lower effective personal tax.

- Non Eligible Dividends: From small business deduction income (~12.2% Ontario rate). 15% gross up, smaller ~9 10% credit, higher personal tax bite.

Example: $100 eligible dividend grosses up to $138, with credits reducing your rate. Always check your corp’s tax paid.

Pros and Cons of Dividends

Pros:

- Skip CPP (~$7K+ savings yearly)

- Often lower personal tax via credits

- Pay anytime profits allow

Cons:

- Zero RRSP room

- No CPP benefits

- TOSI rules may be taxed at high rates if “unreasonable.”

Salary vs Dividends Tax Comparison (Ontario 2026)

“T2 corporate tax vs personal tax” is the battleground. Canada’s integration principle aims for a similar total tax, whether your salary or dividend,d around 45 50% combined at mid levels.

| Factor | Salary | Dividends (Eligible) |

| Corporate Tax | Lower (deductible) | Higher (~26.5%) |

| Personal Tax | Higher (marginal rates) | Lower (w/ credits) |

| CPP | Yes (~$7,668 max) | No |

| RRSP Room | Yes | No |

| Admin Costs | High (payroll) | Low |

Bottom line: Total tax integrates closely, but salary adds retirement perks.

When Salary Is Better (Real Scenarios)

Opt for salary if:

- You crave RRSP growth (e.g., maxing contributions yearly).

- Banks demand it for mortgages (salary = “earned income”).

- CPP retirement appeals (stable post 65 income).

- Your profits are steady, per our T1 personal tax return checklist.

When Dividends Are Better

Go dividends when:

- Short term tax minimization rules (credits beat marginal rates).

- You skip CPP (self fund retirement via investments).

- Flexibility matters (lumpy profits).

- RRSP is maxed, avoiding small business tax deductions pitfalls.

The Best Strategy: Salary + Dividends Mix (Most Important Section)

Why do 80% of savvy accountants recommend blending salary and dividends? It captures the best of both worlds: salary’s retirement perks (RRSP room, CPP) + dividends’ flexibility and tax credits. Pure salary bloats payroll; pure dividends skips future proofing. The mix achieves “perfect integration” similar total tax but superior wealth building.

Step by Step Hybrid Strategy for Hamilton Owners:

- Salary to RRSP Max: Pay yourself up to create full RRSP room (18% of prior earned income, ~$33,540 max in 2026) + CPP max (~$68K salary threshold).

- Dividends for Remainder: Distribute after tax profits as eligible/non eligible based on your T2.

- Timing: Salary quarterly via payroll; dividends anytime (avoid TOSI by documenting reasonableness).

- Annual Review: Adjust for profit changes, family income splitting.

Real Hamilton Example ($250K Corp Profit, Owner in 40% Bracket):

| Component | Amount | Corporate Tax Savings | Personal Tax | RRSP/CPP Benefit | Net Owner Take Home |

| Salary Only | $200K | $24K (deductible) | $92K | $36K room + $7.7K CPP | ~$100K |

| Dividends Only | $200K (eligible) | $0 | $78K (w/credits) | $0 | ~$122K |

| Optimal Mix | $70K salary + $130K dividends | $8K (partial deduct) | $65K | $12K room + $7.7K CPP | ~$133K + retirement boost |

Optimized mix saves ~$10K+ net vs extremes, per 2026 Ontario rates. (Assumes CCPC small business deduction.)

For a $200K profit Hamilton owner: Salary $60K (full RRSP/CPP), dividends $100K post tax. Total tax? ~42% effective plus investments grow tax free.

Pro Tips:

- Use eligible dividends from non SBD income for max credits.

- Income split with family via dividends (watch TOSI).

- Review quarterly to catch small business tax deductions Hamilton owners miss.

Most owners combine both for peak efficiency; don’t go solo. Dive deeper with our guide to finding the best tax accountant in Hamilton, or book Taxmetic for your custom plan.

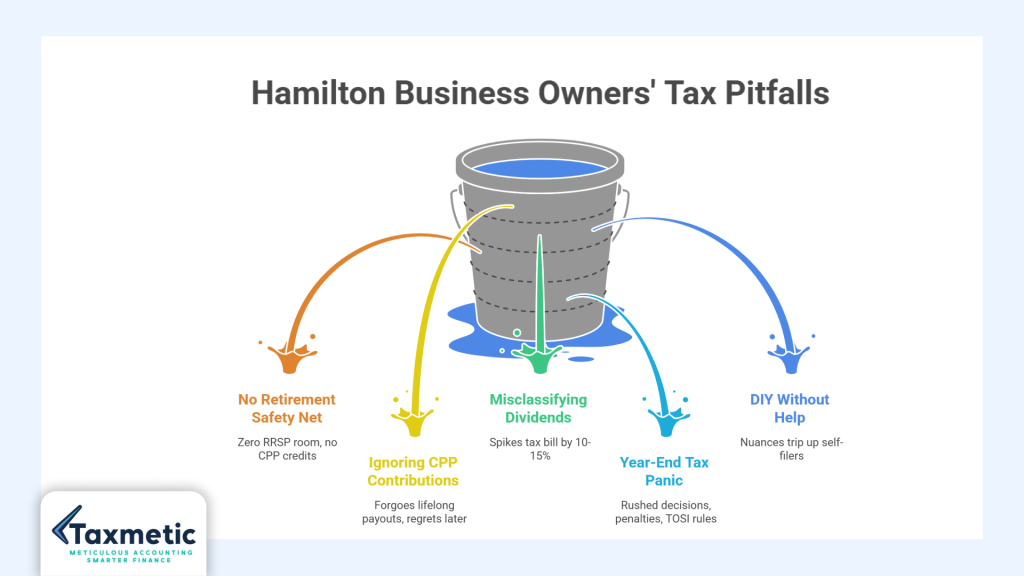

Common Mistakes Hamilton Business Owners Make

Hamilton entrepreneurs often chase short term wins on salary vs dividends, but these pitfalls cost thousands in taxes and missed opportunities. Here’s how to dodge them:

- Taking Only Dividends (No Retirement Safety Net): Many skip salary entirely to avoid CPP and payroll, thinking it’s “tax efficient.” Result? Zero RRSP room and no CPP credits, leaving you scrambling at retirement. In 2026 Ontario rates, that’s ~$33K lost RRSP potential yearly. Fix: Salary to your max RRSP limit first.

- Ignoring CPP Contributions: As owner manager, your corp matches employee CPP, essentially free retirement money. Skipping it for dividends saves ~$7,668 now but forgoes lifelong payouts (up to $1,600/month post 65). Hamilton owners in construction or retail regret this most when profits dip later.

- Misclassifying Eligible vs Non Eligible Dividends: Confusing small business (non eligible, higher personal tax) with general income (eligible, better credits) spikes your bill by 10 15%. Example: $50K non eligible dividends might cost $8K extra vs eligible. Always verify your T2, don’t guess.

- Year End Tax Panic (No Proactive Planning): Waiting until December to decide salary vs dividends means rushed payroll or over dividending, triggering penalties or TOSI rules. Smart Hamilton owners plan quarterly; check our Hamilton business owners tax planning: 5 smart moves for templates.

- DIY Without Professional Help: Googling “dividend vs salary Ontario” feels empowering, but nuances like integration or your marginal rate trip up 70% of self filers. Pros spot $5K+ savings via mixes. Wondering how much does an accountant cost in Hamilton Ontario? It’s cheaper than mistakes start with our secrets to finding the best tax accountant in Hamilton.

Avoid these, and you’ll optimize pay yourself, corporation Canada style, effortlessly.

Salary vs Dividends in Canada (2026): Final Verdict

No one size fits all on salary vs dividends, Canada 2026, it’s personal. Tailor to your income level, business profits, retirement goals, and life stage. High earners ($150K+ profits) thrive on a mix; low profit startups lean on dividends for simplicity.

Quick Decision Framework:

| Your Situation | Best Choice | Why? |

| Profits under $100K | Mostly dividends | Low admin, tax credits offset rates |

| Need RRSP/CPP max | Salary first, then dividends | Builds retirement fast |

| Mortgage/loan coming | Heavy salary | Proves stable income |

| Maxed RRSP, hate admin | Pure dividends | Flexibility + savings |

| $200K+ profits | 40/60 salary dividend mix | Optimal integration |

Hamilton Specific Verdict: With Ontario’s 12.2% small business rate and rising personal brackets (53.53% top), blend salary up to ~$60K (RRSP + CPP sweet spot) and dividend the rest. This dodges TOSI, maximizes credits, and preps for real estate plays vital in our hot market.

Run your numbers: Tools like CRA’s integration calculator show mixes save 5 10% vs extremes. Still unsure? Taxmetic delivers custom plans. Book now and sleep easy.

Frequently Asked Questions:

Q: Should I pay myself a salary or dividends in Canada?

Answer: Depends on RRSP, CPP, and tax goals; most benefit from a mix.

Q: What is the most tax efficient way to pay yourself in Ontario?

Answer: Usually, salary to RRSP max + dividends, balancing integration.

Q: Do dividends avoid tax in Canada?

Answer: No, they’re taxed personally with gross up credits.

Q: Do dividends count as income for mortgages?

Answer: Often, less favorable than salary, lenders prefer “earned” proof.

Q: Can I switch between salary and dividends each year?

Answer: Yes, with planning to avoid TOSI.

Need Help Choosing?

At Taxmetic, we craft personalized compensation strategies for Hamilton owners,s blending salary vs dividends for max savings. From how much does an accountant cost in Hamilton, Ontario, to full planning, book your free consult today.