Real Estate Investor Tax Guide for Hamilton

If you own a rental property in Hamilton, a duplex on the Mountain, a student rental near McMaster, or an Airbnb in the lower city, one thing is becoming impossible to ignore in 2026: the Canada Revenue Agency is paying closer attention to real estate investors than it ever has before.

Hamilton has been one of Southern Ontario’s most active markets for real estate investment over the past decade. Average rents across the city have climbed to roughly $2,069 per month in 2026, up nearly 13 percent year over year, with vacancy sitting at 3.6 percent, which is tighter than the provincial average. Neighbourhoods like Hamilton Mountain and Stoney Creek continue attracting yield-focused investors looking for cash flow that the GTA simply cannot offer at current price levels. Student rentals near McMaster University remain consistently occupied. Duplexes and triplexes across the city are being snapped up by investors who understand the long-term value of owning income-producing property in a city with growing demand and strong fundamentals.

The investment case for Hamilton is still compelling. But what many landlords underestimate is the tax side of the equation, and in 2026, that gap in knowledge is becoming increasingly costly.

The CRA has made rental income compliance a clear enforcement priority. As of 2026, platforms like Airbnb are required to report the income earned by Canadian hosts directly to the CRA. That means the days of unreported short-term rental income slipping through the cracks are effectively over. The CRA has sophisticated data-matching systems and works with platforms like Airbnb to track rental income, and failing to report can result in reassessments going back several years, along with penalties and interest charges.

It is not just Airbnb hosts who need to pay attention. Long-term landlords, property flippers, and investors planning to sell are all facing increased scrutiny. Capital gains rules, principal residence exemptions, HST obligations on short-term rentals, and the proper treatment of renovation costs are all areas where Hamilton investors are making expensive mistakes that a little planning could have prevented.

This guide is written specifically for real estate investors in Hamilton, Ontario. Whether you own one rental unit or a growing portfolio, whether you are renting month to month or listing on Airbnb every weekend, you will find practical and up-to-date information here on how landlord tax in Canada works in 2026, what you are legally required to report, what you can deduct, and how to build a tax strategy that protects your profits rather than eroding them.

Understanding real estate investor tax in Hamilton is not just about staying out of trouble with the CRA. It is about keeping more of what you earn, making smarter acquisition and disposition decisions, and building wealth in a way that is sustainable over the long term. The investors who treat tax planning as part of their investment strategy consistently outperform those who treat it as an afterthought.

Let us start with the foundation.

Understanding Real Estate Taxes in Hamilton Ontario

Before getting into the specific numbers and forms, it helps to understand how rental property is taxed in Canada at a foundational level. Many Hamilton investors jump straight into acquisition without fully understanding the tax framework they are operating within, and that leads to costly surprises later.

How Rental Property Taxes Work in Canada

In Canada, income you earn from a rental property is considered taxable income in the year it is received. This applies whether you own a single basement apartment, a duplex on Concession Street, or a portfolio of properties across the Mountain and Stoney Creek. There is no minimum threshold below which rental income is not reportable. You earned it, you report it.

The CRA draws an important distinction between rental income and active business income. For most landlords, the income they earn falls into the rental income category, which means it is reported on Form T776 (Statement of Real Estate Rentals) and added to your personal income each year. However, if you are operating a property with hotel-like services, such as daily cleaning, linen service, meals, or a front desk arrangement, the CRA may classify your income as business income instead. That distinction changes what forms you file, what expenses you can claim, and whether you need to contribute additional amounts to the Canada Pension Plan.

For investors who own property through a corporation, the income is reported on a corporate tax return (T2) rather than a personal one. This opens up different planning options, which we will discuss later in this guide.

Ontario vs Federal Tax Obligations for Landlords

As a landlord in Hamilton, your tax obligations come from two levels of government, and both need to be addressed each year.

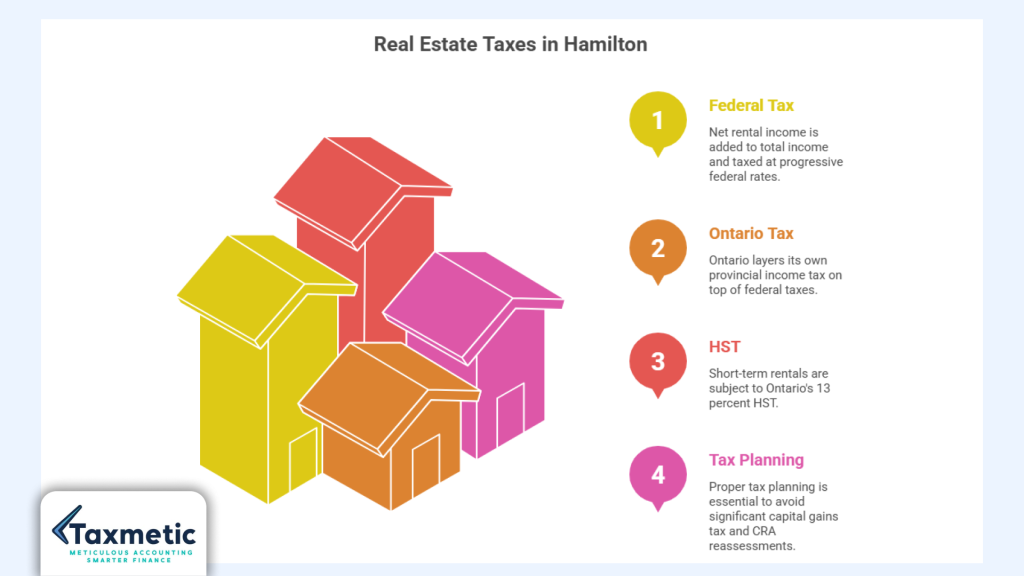

At the federal level, your net rental income is added to your total income and taxed at Canada’s progressive federal income tax rates. In 2026, those rates range from 15 percent on the first $57,375 of taxable income up to 33 percent on income above $246,752. Your net rental income sits on top of whatever else you earned during the year, which can push you into a higher bracket.

Ontario then layers its own provincial income tax on top of that. Provincial rates in Ontario for 2026 range from 5.05 percent to 13.16 percent depending on your total income. This means a Hamilton landlord with a mid-to-high income could be paying a combined marginal rate of over 50 percent on their last dollars of rental income, which makes deductions and tax planning extremely important.

For short-term rental operators, there is a third layer to consider: HST. Long-term residential rentals (leases of one month or more) are exempt from HST in Ontario. However, short-term rentals, meaning stays under 30 consecutive days, are considered a taxable supply under the Excise Tax Act and are subject to Ontario’s 13 percent HST. We will cover this in detail in the Airbnb section below.

Why Hamilton Real Estate Investors Need Proper Tax Planning

Hamilton’s investment appeal is real. The Mountain and Stoney Creek offer strong yields for investors, and demand is driven by GTA migration, McMaster students, and hospital sector workers. Properties that were purchased five or eight years ago have appreciated substantially, even accounting for recent corrections. That is a significant wealth creation story, but it is also a significant tax story.

Without proper planning, an investor who has held a duplex for a decade may find that a significant portion of their gain evaporates to capital gains tax upon sale. A landlord who has been casually mixing personal and rental expenses may face a CRA reassessment that claws back years of deductions. An Airbnb host operating without understanding their HST obligations could find themselves with a large unexpected liability.

The CRA has sophisticated data-matching systems and works with platforms like Airbnb to track rental income, and failing to report can result in reassessments going back several years, along with penalties and interest charges. Good record keeping and proactive tax planning are not optional luxuries. For Hamilton real estate investors in 2026, they are essential.

Rental Income Tax Hamilton: What Landlords Must Report

Do I Pay Tax on Rental Income in Hamilton Ontario?

Yes, absolutely. Every dollar of rental income you earn from a property in Hamilton is taxable under the Income Tax Act, and it must be reported on your annual personal tax return. This applies whether you are renting a basement suite long-term, leasing a full duplex, or collecting short stays through Airbnb. There is no minimum amount that is exempt from reporting, and there is no grace period for new landlords.

The primary form used to report rental income is CRA Form T776, the Statement of Real Estate Rentals. This form walks you through reporting your gross rental income, subtracting your allowable expenses, and arriving at your net rental income or loss for the year. That net figure then flows onto your T1 personal tax return and is added to your other income for the year.

Long-term rentals, meaning leases of one month or longer, make up the bulk of what most Hamilton landlords report. Monthly rent, year-end security deposits that you keep, and any other amounts you receive from tenants all need to be included. If you want to understand more about the personal tax return process itself, the T1 Personal Tax Return Complete Checklist on this website is a helpful starting point.

What Counts as Rental Income?

Many Hamilton landlords underestimate their reportable rental income because they focus only on the monthly rent cheque. The CRA casts a wider net than that. Here is what you need to include:

Monthly rent payments from all tenants, including any amounts received in cash, are the obvious starting point. But beyond that, you also need to report parking fees if you charge tenants separately for parking at your property. Laundry income, if you have coin-operated machines on site, counts as rental income. Any money you receive from Airbnb bookings is rental income, or possibly business income depending on your situation. Security deposits that you legitimately retain at the end of a tenancy because the tenant caused damage are also reportable in the year you keep them. Even amounts a tenant pays on your behalf, such as utilities under a certain arrangement, may need to be included.

The key principle is that rental income is reported on a cash basis. You report it in the year you actually receive it, not the year it is due or invoiced.

Common Mistakes Hamilton Landlords Make

Tax mistakes among Hamilton landlords tend to cluster around a few recurring themes. The most common is not reporting cash rent. Some landlords operate under the mistaken belief that cash transactions are invisible to the CRA. They are not. Tenants in Ontario often claim the Ontario Energy and Property Tax Credit, which requires them to provide landlord details. The CRA cross-references this information regularly.

Mixing personal and rental expenses is another costly mistake. If your rental property expenses run through the same bank account as your personal spending, it becomes very difficult to substantiate your deductions during an audit. What starts as a bookkeeping shortcut can end up costing you far more than it saved in convenience.

Ignoring Airbnb income entirely is a risk that has become significantly greater in 2026. As of 2026, Airbnb is required to report the income earned by Canadian hosts directly to the CRA, and hosts must provide their Social Insurance Number or Business Number to the platform. If you have been operating without reporting, the time to get compliant is now, ideally with professional help to manage any voluntary disclosure process.

Poor bookkeeping ties all these problems together. Without organized records, even legitimate deductions become unclaimed because landlords cannot find the receipts or documentation to support them at filing time. You are entitled to substantial deductions as a rental property owner, but only if you can prove you incurred the expenses.

How CRA Tracks Landlord Income in 2026

The CRA’s ability to identify unreported rental income has expanded substantially over the past few years. Ever since rules governing digital platforms were introduced, Airbnb is required to transmit certain tax information to the CRA, meaning the tax authorities can compare the amounts declared on the platform with those reported on income tax returns.

Beyond platform data sharing, the CRA uses banking records obtained through audit processes, Ontario property tax data, land registry records, and the tenant tax credit information mentioned above. If a tenant claims a rental credit for your property and you have not reported rental income from that property, the discrepancy will surface. The CRA also uses statistical data to flag returns where claimed rental losses seem unusually large or recurring compared to similar properties in the same area.

The risk of audit for Hamilton landlords is real and growing. Working with a qualified real estate accountant in Hamilton who understands CRA’s rental compliance priorities is one of the most practical steps you can take to protect yourself.

Rental Property Deductions Ontario Investors Can Claim

What Can Landlords Deduct in Ontario?

This is where informed landlords gain a significant advantage over those who file carelessly. The CRA allows rental property owners to deduct a wide range of expenses incurred to earn rental income, and those deductions can meaningfully reduce the amount of tax you actually owe. The key is understanding which expenses qualify, keeping documentation for all of them, and applying them correctly against your rental income.

Mortgage Interest vs Mortgage Payments

This is one of the most common points of confusion among Hamilton landlords, and getting it wrong in either direction costs money.

You cannot deduct your full mortgage payment from rental income. A mortgage payment has two components: interest and principal. The interest portion is a deductible expense because it represents the cost of borrowing money to earn income. The principal portion, however, is simply the repayment of money you borrowed, and it is not deductible. Only the interest charges reduce your taxable rental income.

In the early years of a mortgage when interest makes up a larger share of each payment, this distinction is particularly valuable. As the mortgage matures and the interest portion shrinks, the deductible portion decreases accordingly. Your annual mortgage statement from your lender will break out exactly how much interest you paid during the year, and that is the number you carry over to your T776.

Property Expenses You Can Deduct

The following table outlines the most common expenses Hamilton landlords can deduct against rental income:

| Deductible Expense | Allowed? |

| Mortgage interest | Yes |

| Property taxes | Yes |

| Insurance premiums | Yes |

| Repairs and maintenance | Yes |

| Utilities paid by landlord | Yes |

| Property management fees | Yes |

| Accounting and bookkeeping fees | Yes |

| Advertising costs | Yes |

| Landscaping and snow removal | Yes |

| Legal fees related to rental | Yes |

All of these need to be reasonable and directly related to earning rental income. If a property is partially personal use and partially rental, you must prorate expenses accordingly based on the portion used for rental activity.

Capital Expenses vs Current Expenses

Not every dollar you spend on a rental property can be deducted in the year it was spent, and this distinction catches many Hamilton investors off guard.

Current expenses are routine costs of maintaining the property in its existing condition. Repainting walls, fixing a leaky tap, replacing a broken window, or patching a section of drywall after a small repair are all current expenses. These are fully deductible in the year they occur.

Capital expenses, on the other hand, improve the property beyond its original condition or extend its useful life. Replacing an entire roof, installing a new furnace system, adding a new bathroom, or renovating a kitchen are capital expenses. These must be added to the cost of the property (or the relevant class of capital cost) and deducted over time through a mechanism called Capital Cost Allowance, which we touch on in the capital gains section below.

The line between a repair and a renovation can be blurry, and CRA does scrutinize large maintenance deductions closely. If you replaced the kitchen because the cupboards were worn, that is likely a capital expenditure. If you replaced a single broken cabinet door, that is a repair. Getting this classification right matters both for the current year deduction and for any future capital gains calculation when you sell.

Common items that fall into the capital category include appliances for the rental unit, furniture purchased for a furnished suite, window replacements for the whole house, new flooring throughout, and major plumbing upgrades.

Vehicle and Travel Deductions for Landlords

If you use your vehicle to manage your rental properties, a portion of those costs may be deductible. This includes driving to the property to show it to prospective tenants, meeting contractors for repair work, picking up materials, or visiting the property for inspection purposes.

The CRA requires you to maintain a mileage log. This means recording the date, destination, purpose, and kilometers driven for each rental-related trip throughout the year. Without this log, vehicle deductions are extremely difficult to defend in an audit.

You cannot deduct personal vehicle use. Only the portion of kilometers driven for rental business purposes is claimable. At the end of the year, you calculate the rental percentage of your total vehicle use and apply that to your total vehicle costs (fuel, insurance, maintenance, and either depreciation or lease payments).

Home Office Deductions for Real Estate Investors

If you manage your rental properties from a dedicated workspace in your own home, and that space is used exclusively for rental management activities, you may be able to claim a home office deduction. This would cover a proportionate share of your home’s costs: rent or mortgage interest on your own home, utilities, and internet, calculated based on the square footage of the dedicated office space relative to your total home size.

This deduction applies specifically to investors who manage their properties themselves without a property management company and who have a clearly defined workspace at home. It is worth discussing with your accountant at Taxmetic to determine whether your situation qualifies, as the rules around home office claims have specific requirements that must be met. You can also read more on this topic in our Home Office Deduction guide for self-employed Hamiltonians.

Airbnb Tax Ontario: Short-Term Rental Rules for 2026

Short-term rental taxation is one of the fastest-evolving areas of Canadian tax law, and Hamilton investors running Airbnb properties face a layered set of obligations that go well beyond simply reporting income at the end of the year.

Airbnb Tax Rules Ontario 2026

The CRA requires you to report all your Airbnb income, even if you only rent it out every so often. There is no minimum amount. If you are generating rental income, you are legally obligated to include it in your personal tax return.

This applies to every Hamilton host, whether you are renting your spare room on occasional weekends, listing a full property year-round, or anything in between. Airbnb income flows onto your T776 form as rental income (in most cases) and is netted against your allowable deductions before being added to your total income for the year.

From an HST perspective, short-term rentals in Ontario are treated as a taxable supply. The 13 percent HST applies to stays under 30 consecutive days, while long-term residential leases of one month or more are generally HST-exempt. This creates a very real tax split for investors who switch a property between Airbnb and long-term tenancy throughout the year.

Hamilton has its own considerations as well. Investors planning to operate or expand an Airbnb in Hamilton should review the City of Hamilton’s municipal licensing requirements, as bylaws around short-term rentals continue to evolve across Ontario municipalities. Failure to comply with local licensing requirements can have consequences not just with the city, but also with CRA, since for income tax purposes, in order to deduct expenses from a short-term rental property, the property must be compliant, and non-compliant short-term rental properties may have deductions denied.

Short-Term Rental Tax Hamilton Requirements

Hamilton follows Ontario’s broader regulatory framework for short-term rentals, but investors should not assume the rules are identical to those in Toronto or Ottawa. Municipal rules vary across Ontario cities, and some apply a principal-residence-only model that restricts short-term rentals to your primary home.

Most Ontario cities define a short-term rental as any guest stay lasting less than 28 consecutive days. If you rent a property to a tenant for 28 days or longer, the arrangement typically falls under the Residential Tenancies Act, which carries an entirely different set of rules and tenant rights.

For Hamilton investors, the key compliance steps on the municipal side include verifying whether the property is in a zone that permits short-term rentals, confirming whether licensing or registration is required by the city, and ensuring the property meets Ontario Fire Code requirements, including smoke and carbon monoxide detectors on every level and a posted exit plan.

Before you invest in or convert a property to Airbnb use in Hamilton, check directly with the City of Hamilton for the most current bylaws. What is permitted in one neighbourhood may not be in another, and regulations are being updated regularly across Ontario.

When Airbnb Income Becomes Business Income

Most residential Airbnb hosts in Hamilton will report their short-term rental income as property income on Form T776. However, the CRA will reclassify this as business income if your operations start to resemble those of a commercial accommodation provider.

The key signals the CRA looks for include providing hotel-style services to guests such as daily cleaning, linen changes, meal service, or a concierge-type arrangement. If you are regularly on call to provide services to guests beyond basic property access, the CRA may determine you are running a bed-and-breakfast operation, which is business income reported on Form T2125.

Most residential Airbnb hosts fall into property income. Once you hire cleaners, provide breakfast, or offer services resembling a bed-and-breakfast, CRA may reclassify as business income.

The practical consequence of business income classification is that you may need to make CPP contributions on that income, which adds a cost many hosts are not prepared for. The deductible expenses are similar in both categories, but the reporting form and some technical rules differ. If your Airbnb operation is intensive and service-heavy, it is worth discussing the classification with a professional before you file.

HST Rules for Airbnb Hosts in Ontario

If your total annual revenue from Airbnb activities exceeds $30,000 in a 12-month period, you are required to register for and collect GST/HST from your guests. In Ontario, that means adding 13 percent HST to each booking and remitting it to the CRA through regular HST filings.

Once you cross the $30,000 threshold, you have 29 days to register for an HST number. After registration, you are required to file HST returns (monthly, quarterly, or annually depending on your revenue level) and remit the difference between the HST you collected from guests and the HST you paid on your own business expenses, which are called input tax credits.

It is worth noting that the $30,000 threshold combines all your taxable commercial activities, not just Airbnb. If you also freelance or sell goods, those revenues count toward the threshold. You could hit the registration requirement faster than you expect.

For many Hamilton investors who are not yet registered, Airbnb collects and remits HST on their behalf for eligible bookings. However, once you register, you take on the responsibility yourself and must provide your GST/HST number to the platform.

One important note for Hamilton investors considering selling a property that has been heavily used as a short-term rental: if you sell a property used mainly as a short-term rental, the CRA may classify it as a commercial sale, triggering a 13 percent GST/HST charge on the sale price. This applies if the property does not meet the tax definition of a residential property, which can be caused by extensive Airbnb use, furnished short stays, or hotel-like services.

This is a significant consequence that most investors do not see coming. If you plan to sell an Airbnb property, speak with a tax professional well before the sale.

For more context on when you are required to register for HST, our blog on when to register for HST in Ontario covers the rules in detail.

Risks of Converting Long-Term Rentals into Airbnb Properties

Converting a property from long-term tenancy to short-term Airbnb use is a strategy many Hamilton investors are exploring, particularly as rental yields on long-term leases face rent control pressure on existing tenancies. But this conversion carries real tax risks that need to be understood before you act.

When you change the primary use of a property from long-term residential rental to short-term commercial rental, this triggers what the CRA calls a change-of-use. At the point of conversion, you are deemed to have disposed of the property at its current fair market value and to have reacquired it at the same amount. This can generate a capital gain, and depending on your cost base and how much the property has appreciated, the tax consequences can be material.

Additionally, if the property was previously used as a long-term residential rental (HST-exempt), converting it to short-term rental use (HST taxable) means you may need to register for HST and self-assess HST on the fair market value of the property at the time of conversion. This is a nuanced area that requires professional guidance.

The reverse conversion, moving from Airbnb back to long-term rental, can also trigger deemed dispositions. The rules around these conversions are complex enough that getting them wrong is easy, and the cost can be substantial.

Capital Gains Real Estate Hamilton: What Investors Need to Know

How Does Capital Gains Work for Real Estate in Canada?

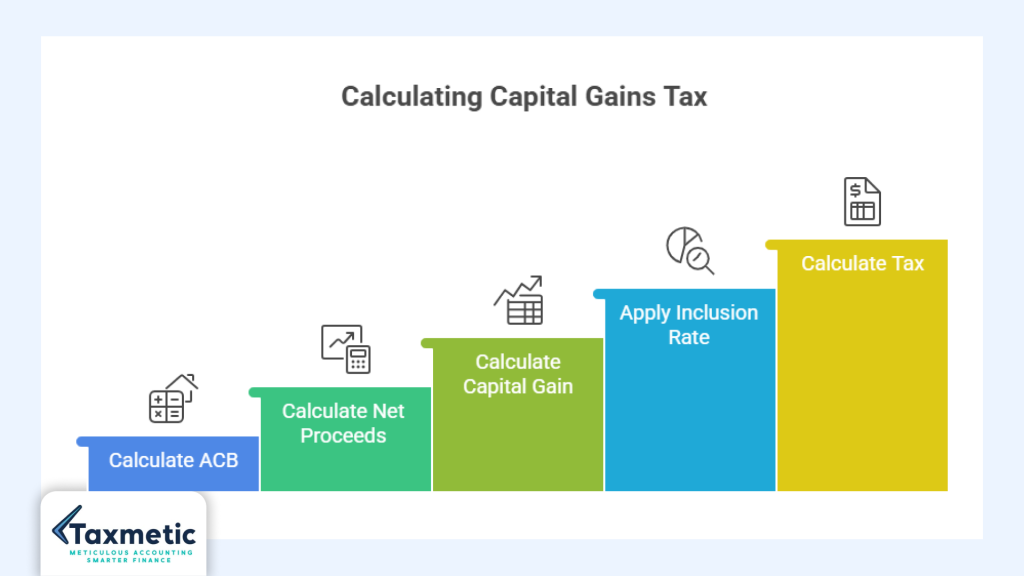

When you sell a rental property in Hamilton for more than you paid for it, the profit is a capital gain. Canada does not have a separate capital gains tax rate. Instead, a portion of your gain is included in your income for the year and taxed at your regular marginal rate.

The gain is calculated as follows: take your sale proceeds and subtract your adjusted cost base (what you effectively paid for and invested in the property) and your selling costs (realtor commissions, legal fees). The result is your capital gain.

As of 2026, Canada’s capital gains inclusion rate remains 50 percent, meaning half of a capital gain is included in income. So if you sell a Hamilton duplex for a $200,000 gain, $100,000 gets added to your income for that year and is taxed at your marginal rate. The other $100,000 is yours tax-free.

2026 Capital Gains Tax Rules in Canada

The capital gains inclusion rate has been the subject of significant political debate over the past two years. The federal government announced that the capital gains inclusion rate would increase from one-half to two-thirds on capital gains realized annually above $250,000 by individuals, effective January 1, 2026. However, this proposed increase was ultimately cancelled, meaning that everyone’s capital gains inclusion rate stays at 50 percent.

For most Hamilton real estate investors selling properties with gains under $250,000, the 50 percent inclusion rate applies straightforwardly. If your gain exceeds that threshold in a single year, the rules above that threshold are still being clarified, so working with a current tax professional for large dispositions is strongly advisable.

The Lifetime Capital Gains Exemption limit has increased to $1.25 million for eligible dispositions, though this applies to qualifying small business shares and farming and fishing property, not to real estate investment properties directly.

One rule introduced in 2023 that remains very much in force for 2026: if you sell a residential property within 365 days of purchasing it, the entire gain is treated as business income, not a capital gain. This means 100 percent of it is taxable, and the principal residence exemption cannot be applied to it either.

How to Calculate Adjusted Cost Base (ACB)

The adjusted cost base is not simply the purchase price you paid. It is a running total of everything you have invested in the property since acquisition, and calculating it accurately can significantly reduce your taxable capital gain.

Your ACB starts with the original purchase price. To that you add: legal fees paid when you purchased the property, land transfer tax paid on acquisition, real estate commissions you paid on the purchase if applicable, the cost of any capital improvements you made over the years (new roof, addition, kitchen renovation, new furnace), and the cost of any other qualifying capital expenditures.

When you sell, you subtract from your proceeds: real estate commission paid to your agent, legal fees on the disposition, any land transfer tax adjustments, and advertising costs directly related to the sale.

The difference between net proceeds and your ACB is your capital gain. Every dollar you can legitimately add to your ACB is a dollar that reduces your taxable gain. This is why keeping receipts for renovations and capital improvements throughout the life of an investment property matters so much.

Capital Gains Example for Hamilton Investors

To make this concrete, consider a practical Hamilton example.

An investor purchased a duplex on Hamilton Mountain in 2016 for $380,000. At the time of purchase, they paid $6,500 in legal fees and $9,500 in land transfer tax. Over the years, they replaced the roof ($18,000), updated the electrical panel ($8,000), and added a new furnace ($6,500). Their total ACB is $428,500.

In 2026, they sell the property for $720,000, paying $28,800 in realtor commissions and $4,200 in legal fees. Their net proceeds are $687,000.

Capital gain: $687,000 minus $428,500 equals $258,500. At a 50 percent inclusion rate, $129,250 is added to their income for 2026. If this investor has combined federal and provincial income from other sources of $120,000, this additional $129,250 pushes their marginal rate to approximately 46 percent on the gain, resulting in roughly $59,455 in tax on the capital gain portion.

Without the renovation costs factored into the ACB, the gain and resulting tax would have been significantly higher.

Recapture of Depreciation (CCA)

If you have claimed Capital Cost Allowance (CCA) on your rental property in previous years, selling the property may trigger what is called CCA recapture. This is one of the most misunderstood advanced tax issues in real estate investing.

CCA is a tax deduction that allows you to claim depreciation on your rental property buildings (not land) over time. It is optional, and many tax advisors recommend against claiming it on rental properties precisely because of the recapture rules. When you sell the property, any CCA you have previously claimed against the asset gets added back to your income as recapture, and unlike capital gains, recapture is included in income at 100 percent, not at the 50 percent inclusion rate.

This means that while CCA reduces your tax bill while you hold the property, it increases your tax bill when you sell. For long-term holders in appreciating markets like Hamilton, this can result in a meaningful recapture amount at sale. The decision to claim CCA or not is a long-term strategy question, and it should be made deliberately with professional guidance, not just claimed automatically because the form allows it.

Principal Residence Exemption Ontario Explained

What Is the Principal Residence Exemption?

The principal residence exemption (PRE) is one of the most valuable tax provisions available to Canadian homeowners. When you sell a property that qualifies as your principal residence for every year you owned it, the entire capital gain is sheltered from tax. You pay nothing.

The exemption is available to Canadian residents who owned and ordinarily inhabited the property as their principal residence during the relevant years. Only one property per family unit (you, your spouse or common-law partner, and unmarried children under 18) can be designated as a principal residence for any given year. The exemption applies on a year-by-year basis, so it is possible to have partial exemption coverage if a property was a principal residence for some years but not others.

The gain is not reported passively. Since 2016, you are required to report the sale of your principal residence on your tax return even if the exemption eliminates all the tax owing. Form T2091 is used to designate the property and calculate the exempt portion. Failure to report can result in the CRA denying the exemption and assessing full capital gains tax on the gain, plus penalties.

Can Landlords Still Qualify for PRE?

Many Hamilton homeowners who rent out a portion of their property worry that doing so automatically disqualifies them from the principal residence exemption. The answer is more nuanced than a simple yes or no.

The CRA generally allows homeowners to maintain their principal residence exemption even when renting out a portion of their home, provided that the rental use is ancillary to the main use of the property as a residence, there are no structural changes to the property to accommodate the rental, and no Capital Cost Allowance is claimed on the property.

A Hamilton homeowner who lives in the main floor of their home and rents the existing basement to a long-term tenant, without adding a separate entrance or doing structural work to create a true self-contained unit, will generally preserve the full principal residence exemption on sale. The rental income needs to be reported annually, but the exemption typically survives.

The CRA generally becomes more concerned when the rental portion exceeds 25 to 40 percent of the total floor area, or when structural changes have been made to create a self-contained unit.

For properties that do not meet these conditions, a partial exemption applies. The gain must be split between the principal residence portion and the rental portion based on square footage or rooms, and capital gains tax applies to the rental portion.

Airbnb and Principal Residence Risks

Converting your primary home into a part-time or full-time Airbnb raises specific risks to your principal residence exemption that many Hamilton homeowners overlook.

When you change a property from personal use to rental, the CRA deems a disposition at fair market value. You may owe capital gains tax on the appreciation to that point, unless you designate the PRE. A Section 45(2) election can be made to defer the deemed disposition, allowing the property to be treated as your principal residence for up to four more years after you stop living in it, even while renting. However, you cannot claim CCA during the period of the election, and it is a one-time election per property.

For Airbnb specifically, the risk is significant if you convert a property from personal residence to primarily Airbnb use. The CRA may view the intensive commercial activity as a change in the fundamental nature of the property, which could trigger a change-of-use and jeopardize the exemption for years after the conversion began. If you eventually sell with what you expect to be a fully exempt principal residence gain, but you operated an Airbnb for several years without proper planning, you could face a very unpleasant reassessment.

The safest approach for Hamilton homeowners who want to use their home for occasional short-term rental is to ensure the rental activity remains genuinely secondary to personal use, avoid structural modifications, and not claim CCA at any point.

Common Misconceptions Ontario Homeowners Have

A widely held misconception is that selling your primary home in Ontario is always tax-free. It can be, but only if the full PRE is available and properly claimed. If you have owned the property for years while also renting it or using it for Airbnb, the exemption may only be partial.

Another common misunderstanding is that the 12-month anti-flipping rule does not apply to principal residences. It does. If you sell a home you have owned for less than 365 days (with limited exceptions for life events like divorce, job relocation, or death), the full gain is treated as business income regardless of whether you lived there.

Some homeowners also mistakenly believe that simply calling a property their principal residence on the sale return is enough. The CRA reviews designation claims, and if the facts do not support the designation (for example, the property was consistently rented out, you owned another home where you actually lived, or the rental portion was substantial), the exemption can be denied.

Working with a knowledgeable accountant when selling any property that has had rental use is the only way to ensure you are maximizing the exemption you are legitimately entitled to, and not claiming more than you qualify for.

Tax Strategies for Hamilton Real Estate Investors

Should You Buy Property Personally or Through a Corporation?

This is one of the most common questions Hamilton real estate investors bring to their accountants, and the honest answer is: it depends on your goals, your income level, and your investment horizon. There is no universally correct answer.

Buying personally is simpler. You report income and losses on your personal T1 return, you can use rental losses to offset other personal income in the same year, and qualifying properties can benefit from the principal residence exemption. The drawback is that your rental income is taxed at your personal marginal rate, which for high-income investors in Ontario can approach or exceed 50 percent on each additional dollar.

Buying through a corporation offers different advantages. The small business tax rate in Ontario on the first $500,000 of active business income is significantly lower than personal marginal rates. However, rental income earned by a private corporation is generally taxed as passive income, which does not benefit from the small business rate and is subject to a higher corporate tax rate, with a refundable tax mechanism called the Refundable Dividend Tax on Hand (RDTOH) that partially recovers tax paid when dividends are distributed.

Corporations also introduce mortgage complexity. Most residential mortgage lenders in Canada will not lend to numbered holding companies for residential rental properties, meaning incorporated investors often need to arrange commercial financing at higher rates or use alternative lenders.

For a comprehensive look at the salary versus dividends and incorporation decision, our blogs on salary vs dividends for business owners and how to incorporate a business in Hamilton are worth reading in conjunction with this guide.

When Incorporation Makes Sense for Landlords

Incorporation generally starts making sense for Hamilton landlords when they are earning rental income they do not need to spend personally right away, because retaining income inside a corporation at a lower tax rate allows the money to compound and grow. It also makes sense when liability protection is a concern, particularly for investors with multiple properties and significant exposure.

If you own a large portfolio, plan to pass properties to the next generation, or want to engage in more sophisticated income-splitting strategies, corporate structures (sometimes with a management company arrangement) can provide meaningful long-term tax advantages.

However, incorporation is not a simple or inexpensive step. There are setup costs, ongoing legal and accounting fees, the need for separate banking and bookkeeping, and complex rules around extracting money from the corporation. The decision should always be made after a full analysis of your specific situation with a qualified advisor who understands both real estate and corporate tax law.

Record Keeping Tips for Ontario Investors

Good records are the foundation of every successful tax strategy for Hamilton landlords. Without them, you cannot claim deductions, you cannot defend yourself in an audit, and you cannot calculate your adjusted cost base accurately when the time comes to sell.

Maintain a separate bank account and credit card exclusively for rental property activity. This one habit alone makes the bookkeeping process significantly cleaner and reduces the risk of personal expenses being mixed in.

Keep all receipts. In 2026, this is easier than ever with apps that photograph and categorize receipts in seconds. Whether it is a receipt for a can of paint, a plumber’s invoice, or a property management fee, save it digitally with a clear description of what it relates to.

Track your mileage for every rental-related drive using a mileage app or a written log. Record the date, starting and ending point, purpose, and kilometers.

File your T776 annually with accurate gross revenue and all eligible expenses claimed. Do not leave deductions on the table because you did not organize your records.

Review your property’s capital cost additions every year. Every renovation and capital improvement that qualifies should be added to your ACB records at the time it is incurred, not reconstructed from memory years later when you go to sell.

For bookkeeping software options tailored to small business and investment property owners in Hamilton, our comparison of Xero vs Wave vs QuickBooks is a practical resource to help you choose the right tool.

Why Working with a Real Estate Accountant Hamilton Investors Trust Matters

Rental property taxation in Hamilton involves a lot of moving parts. The rules around short-term rentals, capital gains, HST, the principal residence exemption, and corporate structures are genuinely complex, and they interact with each other in ways that require expertise to navigate well.

A qualified real estate accountant who understands Hamilton’s market and Canada’s tax laws can help you structure your investments more efficiently, identify deductions you might miss, make the right decisions around CCA claiming, plan for dispositions before you sell, and stay compliant with the CRA’s evolving requirements.

The cost of good tax advice is itself a deductible expense against your rental income. It is also far less than the cost of a CRA reassessment, a missed deduction, or a poorly planned property sale.

If you own rental property in Hamilton and have never sat down with a tax professional who specializes in real estate investor tax, 2026 is a good year to make that conversation happen.

CRA Audit Triggers Real Estate Investors Should Avoid

Red Flags That Increase Audit Risk

CRA audits of rental property owners are common, and they tend to follow predictable patterns. Understanding what draws attention is the first step to avoiding it.

Claiming large rental losses year after year is one of the clearest signals. Every rental investment has startup costs and occasionally lean years, but if your property consistently shows a substantial net loss on paper while you are also claiming it generates significant income in other ways, the CRA will question whether a reasonable expectation of profit exists. You can read more about CRA audit red flags in our dedicated guide on CRA audit triggers in Canada.

Unreported Airbnb income is now one of the highest-risk areas, given the platform reporting rules introduced in 2026. If your Airbnb transaction summary shows $40,000 in gross earnings but your tax return shows nothing from that property, the CRA’s data-matching will flag this.

Excessive deductions relative to rental income raise questions. Claiming 95 percent of your property costs as rental expenses when only 40 percent of the space is rented, or deducting personal renovation costs as rental repairs, will draw scrutiny.

Misclassifying capital expenditures as current repairs is another common trigger. A $30,000 kitchen renovation claimed as a maintenance repair in a single year will get attention.

Missing documentation is the final common issue. CRA can accept or reject deductions based on whether you can prove them. Without receipts, invoices, contracts, and bank records, even legitimate expenses may be disallowed.

Documents Landlords Should Keep

The following documentation is essential for every Hamilton rental property owner:

Mortgage statements showing interest paid each year. These form the basis of your largest and most valuable deduction. Property tax notices from the City of Hamilton. Insurance policy documents and annual premium statements. All repair and maintenance invoices with the contractor’s name, address, and date of work. Lease agreements for every tenant, including any renewals or amendments. Airbnb transaction summaries and payout records. Utility bills if you pay utilities on behalf of tenants. Capital improvement receipts, including contractor invoices, permits, and inspection records. Your mileage log if you claim vehicle expenses. Any property management agreements and fee statements.

The CRA can generally audit returns up to three years back from the date of assessment. In cases of misrepresentation or fraud, that window extends to six years or more. Keeping your records for a minimum of six years from the filing date is a prudent standard for rental property investors.

Real Estate Tax Checklist for Hamilton Investors (2026)

Use this checklist at the end of each tax year to make sure nothing has fallen through the cracks:

- Report all rental income, including cash payments, parking fees, laundry revenue, and Airbnb earnings, on Form T776.

- Confirm you have separated capital expenditures (roof, furnace, renovations) from current repair expenses and recorded them correctly.

- Track your mileage for every rental-related vehicle trip during the year and ensure your log is complete.

- Save all receipts and invoices for every rental-related expense, organized by property.

- Review your HST obligations. If your Airbnb or short-term rental revenue has crossed or is approaching the $30,000 threshold over four consecutive quarters, confirm whether you are registered and filing correctly.

- Calculate your adjusted cost base accurately, including all capital improvements made during the year, so your records are current if you sell.

- Review your Airbnb compliance with Hamilton’s municipal bylaws and Ontario’s provincial regulations.

- Confirm that any principal residence claims are properly documented if you also rent part of your home.

- Review whether you claimed CCA in previous years and what the recapture implications would be if you sell this year.

- Speak with your accountant if any major transactions occurred during the year, including purchases, sales, conversions, or financing changes.

Frequently Asked Questions

Q: Do I Pay Tax on Rental Income in Hamilton Ontario?

Answer: Yes. All rental income from Hamilton properties is taxable and must be reported on CRA Form T776 as part of your annual T1 personal tax return. There is no minimum threshold, and there are no exemptions for small amounts or occasional rentals.

Q: What Can Landlords Deduct in Ontario?

Answer: Ontario landlords can deduct mortgage interest, property taxes, insurance, utilities, repairs and maintenance, property management fees, accounting fees, advertising costs, and a proportionate share of vehicle and home office expenses if applicable. Capital improvements must be added to your ACB rather than deducted in full in the year incurred.

Q: Is Airbnb Income Taxable in Canada?

Answer: Yes. Airbnb income is fully taxable regardless of how frequently you rent or how much you earn. It must be reported each year, and as of 2026, Airbnb shares host income data directly with the CRA.

Q: Do I Need to Charge HST on Airbnb in Ontario?

Answer: If your total annual revenue from Airbnb activities exceeds $30,000 in a 12-month period, you are required to register for and collect GST/HST from your guests. Short-term stays under 30 days are subject to Ontario’s 13 percent HST. If you are not registered, Airbnb may collect and remit HST on your behalf.

Q: How Can I Reduce Capital Gains Tax on Rental Property?

Answer: The most effective strategies include maximizing your adjusted cost base by documenting all capital improvements accurately, timing the sale to a lower-income year where possible, using capital losses from other investments to offset the gain, and considering the principal residence exemption if applicable. For large portfolios, estate planning strategies and potential use of corporate structures may also reduce the overall tax burden.

Q: Can I Avoid Capital Gains with the Principal Residence Exemption?

Answer: Only if the property genuinely qualifies as your principal residence. A property you have always rented to tenants does not qualify. A property you lived in for some years and rented for others may qualify for a partial exemption. A property you used extensively as an Airbnb may have exemption complications. Speak with your accountant before making assumptions about exemption eligibility.

Q: Should I Incorporate My Rental Property Business?

Answer: It depends on your income level, investment goals, and whether you plan to retain earnings inside the corporation rather than distribute them immediately. Incorporation is not always advantageous for rental income specifically, but it can make sense in certain circumstances. Our blogs on salary vs dividends and how to incorporate in Hamilton provide useful context, but a personalized analysis with a tax professional is always the right first step.

Conclusion

Real estate taxes in Hamilton are manageable with the right approach. The rules around rental income, Airbnb obligations, capital gains, and the principal residence exemption are detailed, but investors who plan ahead, keep organized records, and work with qualified professionals consistently keep more of what they earn.

CRA enforcement in 2026 is stronger than ever. Platform reporting and data-matching mean the cost of getting this wrong is real. But so are the legal tools available to reduce your tax burden, from deductions and ACB planning to disposition timing and exemption strategies.

At Taxmetic, we help Hamilton landlords, real estate investors, and Airbnb operators build tax strategies that protect their returns year after year.