Home Office Deduction Canada: What Self-Employed Hamilton Residents Can Actually Claim

If you run your business from home in Hamilton, you are leaving real money on the table by not claiming every home office expense you are legally entitled to. The Canada Revenue Agency allows self-employed individuals to deduct a portion of their home costs as a business expense, but the rules are specific, and the mistakes people make when filing these claims are surprisingly common.

In 2026, this deduction matters more than ever. The way people work has fundamentally shifted. Hamilton has seen a steady rise in freelancers, independent consultants, mortgage brokers, healthcare practitioners working from private home clinics, real estate agents, digital agency owners, and sole proprietors who run their entire operation from a dedicated home office. What used to be an occasional work-from-home situation has become a permanent business model for thousands of Ontario residents.

At the same time, the CRA has sharpened its focus on home office claims. Inaccurate home office calculation, inflated square footage, and improperly claimed expenses are among the most common reasons self-employed individuals receive review notices or audit flags. If you want to learn more about which financial decisions tend to attract CRA attention, our blog on CRA audit red flags in Canada covers eight of the most common triggers that put taxpayers on the agency’s radar.

One thing that causes a lot of confusion is the difference between how employees and self-employed individuals claim home office deduction expenses. Employees who received a T2200 form from their employer during the pandemic years became familiar with the concept, but the rules for them are far more restrictive. Self-employed individuals file under Form T2125, which covers business-use-of-home expenses, and they generally have access to a broader list of deductible costs. If you are a sole proprietor, contractor, or freelancer, you are not bound by the same limitations as someone on payroll.

This guide is written specifically for Hamilton business owners and self-employed professionals who want a clear, practical breakdown of what the home office deduction Canada actually covers, how to calculate home office deduction correctly, what documentation CRA expects, and where people commonly go wrong. Whether you are working out of a finished basement in Ancaster, a spare bedroom in the East End, or a condo home office in downtown Hamilton, the principles here apply directly to your situation.

Can Self-Employed People Claim Home Office Expenses in Canada?

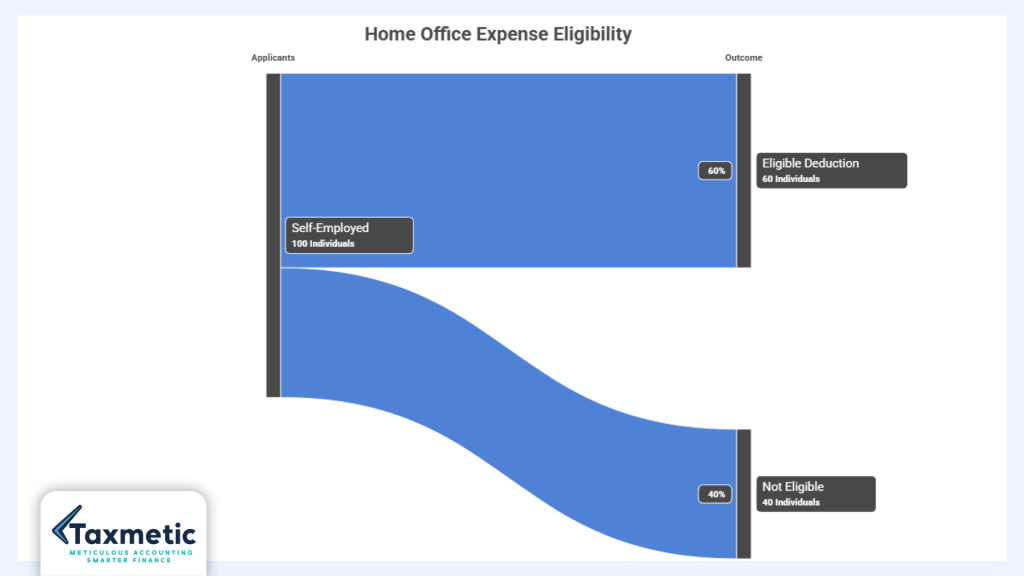

The short answer is yes, and for many Hamilton self-employed professionals, this deduction can translate into hundreds or even thousands of dollars in reduced taxable income each year. But eligibility is not automatic. The CRA has specific requirements you need to meet before you can deduct any portion of your home costs as a business expense.

When you are self-employed, your home office costs fall under what the CRA calls “business-use-of-home expenses.” These are reported on Form T2125, which is the Statement of Business or Professional Activities that sole proprietors and unincorporated business owners file alongside their T1 personal tax return. This is a completely different process from the T2200 route that employees use, and it comes with different rules and different eligibility for home office deduction expenses.

The key distinction is this: employees need their employer to certify that they were required to work from home deduction. Self-employed individuals answer only to the CRA’s eligibility criteria, which gives you more control but also more responsibility to get it right.

To qualify for the business-use-of-home deduction as a self-employed person in Canada, your home workspace must meet at least one of the following conditions:

The workspace is your principal place of business, meaning it is where you carry out the majority of your work activities. Or, the workspace is used exclusively and on a regular and continuous basis for meeting clients, customers, or patients as part of your business.

If your situation meets either of these conditions, you are eligible to claim a proportional share of your home office deduction expenses against your business income. Getting this right starts with understanding exactly what the CRA looks for when it evaluates these claims.

CRA Rules for Home Office Deduction Canada

Ontario’s self-employed community has grown significantly over the past several years, and with it, the number of home office claims filed each tax season. The CRA applies consistent national rules to these claims, but local context matters. A freelancer working from a 900 square foot Hamilton condo faces a very different home office calculation than a consultant operating from a 2,500 square foot home in Dundas. Understanding how the CRA evaluates these claims helps you file accurately and confidently.

The “Principal Place of Business” Test

The most commonly used eligibility route for self-employed individuals is proving that their home is their principal place of business. CRA interprets this to mean that more than 50 percent of your total working time is spent in that home workspace.

For a Hamilton-based freelance writer, graphic designer, bookkeeper, or online consultant who has no commercial office and conducts all their work from home deduction, this test is usually straightforward to satisfy. You work from home. That is your business location.

The situation becomes more nuanced for professionals who split their time between client sites and home. A contractor who spends three days a week on-site and two days working from their home office in Hamilton may not automatically qualify under the principal place of business test. In that case, the second eligibility route, the client meeting requirement, becomes relevant.

The Dedicated Space Requirement

This is one of the most misunderstood aspects of the home office deduction Canada. The CRA does not require you to have a separate room with a locked door, but it does expect the space to be used exclusively or primarily for business purposes.

A proper home office that qualifies might look like a spare bedroom converted into a workspace, a finished basement used solely for your business, or a defined area of your home that is clearly set up as an office with a desk, filing systems, and business equipment.

What generally does not qualify is the kitchen table where you occasionally open your laptop, the living room couch you use to answer emails in the evenings, or a bedroom that doubles as your workspace on busy days. These spaces fail the dedicated use test because their primary function is personal, not business.

For Hamilton entrepreneurs working in smaller homes or condos, this is a real challenge. If your workspace is a defined corner of your living room with a dedicated desk, you can make a reasonable case for it, but you need to be realistic about the square footage you are claiming and be prepared to explain the setup if CRA ever asks.

Hybrid Work Situations in Ontario

The rise of hybrid work has introduced a grey area that many Ontario self-employed professionals are navigating right now. If you are self-employed and work partly from home and partly from a co-working space, a client’s office, or a commercial location, your eligibility for the home office deduction Canada depends on how you structure your time and where the majority of your business activity takes place.

What typically qualifies: A consultant who works from their Hamilton home office four days a week and visits clients one day a week can generally still claim the home office deduction Canada, as their home remains the principal place of business.

What typically does not qualify: A self-employed professional who rents a full-time commercial office and occasionally works from home on evenings or weekends would have difficulty justifying a home office deduction Canada, since the commercial location is the actual principal place of business.

The hybrid work home office situation in Ontario requires honest self-assessment. If your home workspace genuinely serves as the base of your operations, document it accordingly. If it is supplementary to a commercial location, the deduction likely does not apply.

What Home Office Expenses Can You Claim?

This is where the home office deduction Canada becomes genuinely valuable for self-employed Hamilton residents. The list of eligible expenses is broad, and when you apply your home office percentage to a full year of costs, the deductible amount can be substantial.

Eligible home office deduction Canada Expenses

The following expenses are eligible for self-employed individuals who qualify for the business-use-of-home deduction:

Rent: If you rent your home, a proportional share of your monthly rent is deductible. This is one of the most straightforward and commonly claimed expenses.

Utilities: Heat, electricity, and water costs are all eligible. Your utility bills from Hamilton Hydro, Enbridge Gas, or your water provider can all be included in your home office calculation.

Internet: Your home internet bill is deductible as a home office expense. Given that most modern businesses rely entirely on internet connectivity, this is a particularly relevant deduction for Hamilton digital professionals, consultants, and remote workers.

Property taxes: If you own your home, your annual property tax bill is included in the eligible expense pool. Hamilton property taxes, which have increased in recent years, can make this a meaningful addition to your deductible total.

Mortgage interest: This is one area where self-employed individuals have an advantage over employees. You can claim the interest portion of your mortgage payments as a home office expense. Note that this is interest only, not the principal repayment.

Home insurance: Your homeowner’s or tenant’s insurance premium is eligible on a proportional basis.

Maintenance and repairs: General home maintenance costs, such as cleaning services, minor repairs, and upkeep that applies to the whole home, are eligible. However, repairs or renovations that are specific to your home office are treated differently and may be fully deductible or classified as capital expenses depending on the nature of the work.

It is equally important to understand what you cannot claim. Capital expenses, which are improvements that increase your home’s value such as a full basement renovation or a home addition, are not deductible as current year home office deduction expenses. Personal use expenses that have no business connection are also excluded. And any expense that relates entirely to the non-business areas of your home cannot be included in the home office calculation.

The table below shows how the deductible expenses differ between self-employed individuals and employees, which is a distinction that causes significant confusion every tax season.

| Expense Type | Self-Employed | Employees |

| Rent | Yes | Sometimes |

| Mortgage Interest | Yes | No |

| Utilities (Heat, Hydro, Water) | Yes | Yes |

| Property Tax | Yes | Limited |

| Home Insurance | Yes | No |

| Internet | Yes | Yes |

| Maintenance and Repairs | Yes (general) | Limited |

| Furniture and Equipment | Usually No | No |

| Capital Improvements | No | No |

If you want to see how home office deduction expenses fit into the broader picture of what you can write off as a self-employed professional, our blog on small business tax deductions that Hamilton owners miss covers several other categories that often go unclaimed.

How to Calculate Home Office Deduction Canada

Getting the home office calculation right is critical. The CRA does not prescribe a single formula, but the square footage method is the most widely accepted approach and the one most likely to withstand scrutiny if your return is ever reviewed.

Step 1: Measure Your Workspace

Start by measuring the floor area of your dedicated home office in square feet. Use the actual usable space, which means the room itself without closets unless those closets are used for business storage. Be precise. If your office is 12 feet by 11 feet, your workspace is 132 square feet.

Then measure the total square footage of your home. Include all finished, livable space. Unfinished basements and attached garages are typically excluded unless they are part of your working area.

Step 2: Calculate Your Home Office Percentage

Divide your workspace area by the total home area and multiply by 100 to get your business-use percentage.

Home Office Percentage = (Workspace Area divided by Total Home Area) multiplied by 100

For example: A Hamilton freelancer works from a dedicated office of 150 square feet in a home that totals 1,500 square feet.

150 divided by 1,500 equals 0.10, multiplied by 100 equals 10 percent.

This means 10 percent of eligible home expenses can be claimed as a business deduction.

Step 3: Apply Your Percentage to Eligible Expenses

Once you have your home office percentage, apply it to each eligible expense you incurred during the tax year. The result is your deductible home office amount for that expense.

| Expense | Annual Cost | Deductible Percentage | Claim Amount |

| Rent | $24,000 | 10% | $2,400 |

| Utilities | $3,000 | 10% | $300 |

| Internet | $1,200 | 10% | $120 |

| Property Tax | $5,000 | 10% | $500 |

| Home Insurance | $1,800 | 10% | $180 |

| Total Deduction | $3,500 |

That is $3,500 in home office deduction expenses from a modest 10 percent business-use ratio. For someone in a higher tax bracket, this could represent over $1,000 in actual tax savings.

Shared Space home office calculation Example

If your workspace is not exclusively used for business, such as a guest room that also contains your desk and business equipment, you need to apply a second adjustment based on the proportion of time the space is used for business purposes.

For example: A room that is 200 square feet is used for business 60 percent of the time and personal use 40 percent.

Business-use area for home office calculation purposes would be 200 multiplied by 0.60, which equals 120 effective square feet.

You would then use 120 square feet rather than 200 square feet when calculating your home office percentage. This time-based adjustment is important for anyone working in a shared space and is something CRA may ask you to justify.

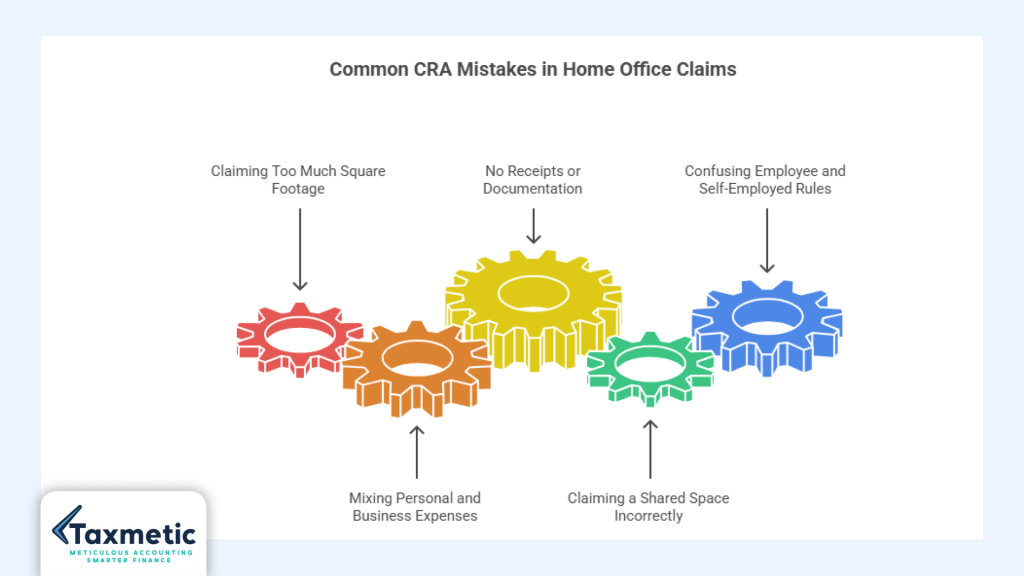

Common CRA Mistakes That Trigger Reviews

Home office claims are one of the more closely examined areas of self-employed tax returns. The CRA has seen enough questionable claims to know where to look. Avoiding these mistakes is not just about compliance; it is about protecting yourself from a stressful review process that can result in reassessments and penalties.

Claiming Too Much Square Footage

This is the most common error. A homeowner might estimate their office at 250 square feet when it is actually closer to 150, or they include hallways, bathrooms, and storage areas in their workspace measurement. CRA can and does ask for floor plans or photos to verify claims. If your numbers do not reflect reality, the reassessment will.

Practical example: A Hamilton consultant operating from a finished basement claims the full basement as their office. However, only one room in that basement is actually used for business. The utility room, laundry area, and storage space should not be included in the workspace measurement.

Mixing Personal and Business Expenses

Some expenses have a personal component that must be separated before you apply your business-use percentage. For example, if your internet plan is also used by your family for streaming and gaming, and you are applying 100 percent of the bill as a home office expense without first accounting for personal use, that is an overstatement that could attract attention.

No Receipts or Documentation

A surprisingly large number of self-employed individuals claim home office expenses without keeping the actual invoices and statements to back them up. CRA does not accept estimates or memory. If you cannot produce a utility bill, a property tax statement, or a rent receipt, you cannot defend the claim.

Claiming a Shared Space Incorrectly

Using your dining table or kitchen counter as a workspace and claiming the entire open-plan living and dining area as your home office is a common mistake that does not hold up to scrutiny. The space needs to have genuine business-use characteristics. A dining room used for family meals cannot be claimed as a dedicated workspace even if you also work there occasionally.

Condo workspace situations are particularly tricky. In a 700 square foot Hamilton condo, claiming 30 percent as your home office when you have an open-concept layout with a small desk area is likely to raise questions. Be realistic and conservative in your estimates.

Confusing Employee and Self-Employed Rules

Some people who were employees working from home during the pandemic years, and who became familiar with the temporary flat-rate method or the T2200 process, mistakenly apply employee-based rules to their self-employed situation, or vice versa. The two systems are entirely separate. Self-employed individuals report on T2125. Employees file through Schedule 1 with T2200 support from their employer. Mixing these up can result in disallowed claims or missed deductions.

For a deeper look at what typically triggers a CRA review, the CRA audit red flags in Canada blog covers this topic in detail and is worth reviewing before you file.

Home Office Deduction Canada Examples for Hamilton Self-Employed Workers

Abstract rules are easier to understand when they are applied to real situations. The following examples use realistic Ontario figures to show how the home office deduction Canada works in practice for different types of Hamilton self-employed professionals.

Freelance Graphic Designer

A freelance graphic designer lives in a rented two-bedroom apartment in Hamilton’s Beasley neighbourhood. Monthly rent is $1,950. The apartment is 950 square feet, and the second bedroom used exclusively as a studio and design workspace is 130 square feet.

Home office percentage: 130 divided by 950 equals 13.7 percent.

Annual eligible expenses include rent ($23,400), utilities ($2,400), and internet ($1,080), totalling $26,880. At 13.7 percent, the total home office deduction Canada comes to approximately $3,683.

Mortgage Broker Working From Home

A self-employed mortgage broker in the Hamilton Mountain area owns a 1,800 square foot home and uses a 180 square foot dedicated office to meet clients, review applications, and manage files. The mortgage broker meets clients in this space regularly, satisfying the CRA’s client-meeting requirement.

Home office percentage: 180 divided by 1,800 equals 10 percent.

Annual eligible expenses include mortgage interest ($9,600), property tax ($6,200), utilities ($3,600), insurance ($1,900), and internet ($1,200), totalling $22,500. At 10 percent, the deductible amount is $2,250.

Online Consultant

A business consultant in Ancaster runs a fully remote consulting practice from a dedicated office in their 2,100 square foot home. The office measures 210 square feet. All client meetings take place via video call. The home is their principal place of business.

Home office percentage: 210 divided by 2,100 equals 10 percent.

Annual eligible expenses: mortgage interest ($14,400), property tax ($7,800), utilities ($4,200), internet ($1,440), insurance ($2,100), totalling $29,940. At 10 percent, the deductible amount is $2,994.

Real Estate Professional

A self-employed real estate agent in Stoney Creek rents a 1,200 square foot townhouse and uses a 144 square foot second bedroom as a dedicated home office for paperwork, client follow-ups, and virtual showings. Monthly rent is $2,100.

Home office percentage: 144 divided by 1,200 equals 12 percent.

Annual eligible expenses: rent ($25,200), utilities ($3,000), and internet ($1,200), totalling $29,400. At 12 percent, the deductible amount is $3,528.

These examples show that even modest home office percentages applied to typical Ontario housing costs can produce meaningful tax deductions. If you are unsure how your situation compares, our self-employed in Hamilton 2026 tax guide walks through the broader filing landscape for Hamilton sole proprietors.

What Records Should You Keep for CRA?

One of the least glamorous but most important parts of claiming home office expenses is documentation. The CRA can review your return for up to three years after the original filing date in most cases, and sometimes longer if they suspect misrepresentation. That means a claim you make today might need to be justified years from now.

Good record-keeping is not about being paranoid. It is about being prepared. The types of records you should retain include:

Utility bills: Keep monthly statements for electricity, gas, and water for the full tax year. Digital copies saved to a cloud folder work well.

Rent receipts: If you rent your home, obtain receipts or written confirmation from your landlord showing monthly payments. A bank statement showing regular rent transfers can also serve as supporting documentation.

Mortgage statements: Keep your annual mortgage statement showing the breakdown between principal and interest. Only the interest portion is deductible, so this document is essential.

Internet invoices: Retain monthly or annual invoices from your internet provider. These are often available through online account portals.

Property tax notices: Your City of Hamilton property tax bill shows your annual amount. Keep the notice and any payment confirmation.

Home insurance documents: Keep your annual policy renewal showing the premium amount.

Floor plan or measurements: Sketch or document the square footage of your home office and total home. If you have a floor plan from when you purchased or rented the property, keep it. Taking your own measurements and documenting them in writing is also acceptable.

Photos of your workspace: Take dated photographs of your home office setup. This provides visual evidence that a dedicated, legitimate workspace exists.

Business calendars or logs: If your workspace qualifies through the client meeting requirement rather than the principal place of business test, keep records of when clients visited and what the meetings were for.

Store these records for a minimum of six years from the end of the tax year to which they relate, which is the CRA’s standard retention recommendation for business records.

Can Incorporated Business Owners Claim Home Office Expenses?

The home office deduction Canada discussion so far has focused on sole proprietors and unincorporated self-employed individuals. If you have incorporated your Hamilton business, the rules work quite differently, and this distinction matters significantly for your tax planning.

A corporation is a separate legal entity from you as an individual. Your home belongs to you, not to your corporation. Because of this, your corporation cannot directly claim home office expenses against its income the way a sole proprietor can on Form T2125.

There are two main ways incorporated business owners in Ontario approach this situation:

Shareholder reimbursement: You as the business owner track your home office expenses and submit an expense claim to your corporation. The corporation reimburses you for the business-use portion of your home costs. This reimbursement is a deductible business expense for the corporation and is generally not taxable income to you as a shareholder, provided the amounts are reasonable and properly documented.

Paying yourself a rent allowance: Some incorporated business owners charge their corporation a reasonable rent for the use of their home office space. The rent paid by the corporation is deductible for the business, but you must report it as rental income on your personal return. This approach introduces additional complexity and CRA scrutiny, because the rent amount must reflect fair market value and the arrangement must be properly structured.

Both approaches require careful documentation and ideally the guidance of an accountant familiar with incorporated small businesses in Ontario. Getting this wrong can result in the reimbursement being treated as a taxable shareholder benefit, which creates unexpected personal income tax obligations.

If you are trying to decide between operating as a sole proprietor or incorporating, our blog on how to incorporate a business in Hamilton gives a thorough breakdown of what incorporation actually involves and when it makes sense. And if you are already incorporated and working through how to pay yourself efficiently, the salary vs dividends article addresses one of the most important decisions incorporated owners face.

Professional bookkeeping becomes especially important for incorporated business owners navigating home office reimbursements. Without proper records and clear separation between personal and corporate finances, these claims can create complications that far outweigh the tax savings.

When to Talk to a Tax Professional

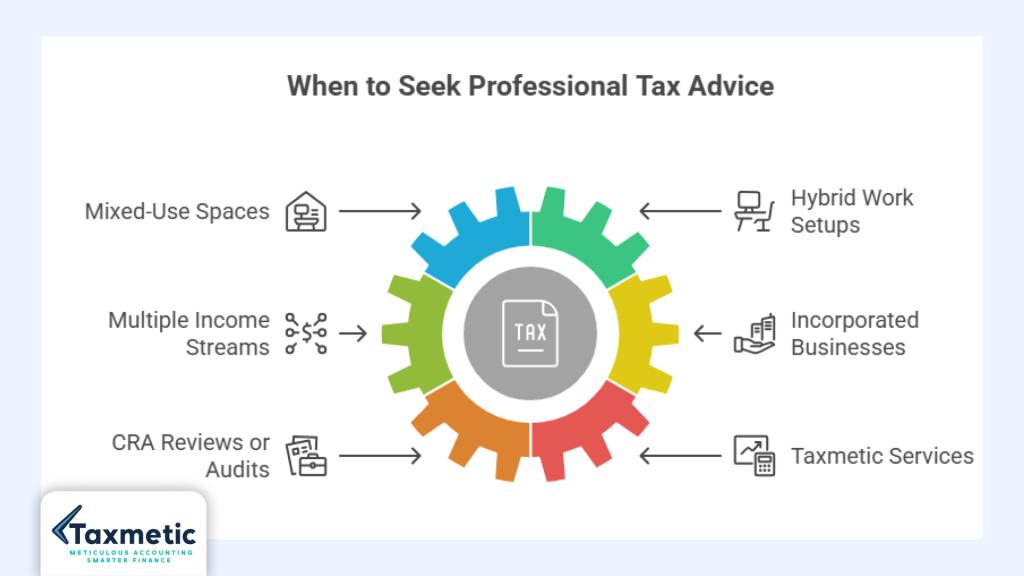

The home office deduction Canada is one of those areas where the general rules seem straightforward but the specific application to your situation can get complicated quickly. There are several circumstances where working with a tax professional is not just helpful but genuinely important.

Mixed-use spaces: If your workspace serves dual purposes, such as a guest room that is also your office, or a studio that is used for both business and personal creative work, calculating the correct deductible portion requires careful analysis. Getting it wrong in either direction, claiming too much or missing legitimate deductions, has real consequences.

Hybrid work setups: If you split your work time between a home office and a commercial location, or if your business structure changed during the year, a professional can help you determine whether you qualify for the deduction and how to calculate home office deduction accurately.

Multiple income streams: Many Hamilton self-employed professionals have more than one source of business income. A real estate agent who also runs an online course, or a consultant who also does freelance writing, may need to allocate home office expenses across multiple income streams on their T2125 forms. This requires precision and knowledge of how CRA expects multi-activity situations to be reported.

Incorporated businesses: As covered in the previous section, incorporated business owners face a more complex set of rules around home office reimbursements, and the cost of getting this wrong is higher than for a simple sole proprietorship situation.

CRA reviews or audits: If you have received a letter from the CRA questioning your home office claim, or if you are concerned that a past return may have overstated your deductions, professional guidance is essential before you respond.

Taxmetic works with Hamilton self-employed professionals, freelancers, and small business owners to make sure their home office claims are accurate, well-documented, and fully optimized within CRA guidelines. Whether you are filing your first return as a self-employed person or you have been claiming these deductions for years and want a second opinion, having a knowledgeable team review your situation is one of the best investments you can make at tax time.

For more on what to look for when choosing the right tax professional for your business, our blog on finding the best tax accountant in Hamilton is a useful starting point. And if you are weighing the cost of professional help, our breakdown of how much an accountant costs in Hamilton, Ontario puts those numbers in practical context.

Frequently Asked Questions

Q: Can self-employed people claim home office expenses in Canada?

Answer: Yes. Self-employed individuals in Canada can claim home office expenses under the business-use-of-home category, reported on Form T2125. To qualify, your home workspace must either be your principal place of business, meaning you perform more than 50 percent of your work there, or it must be a space you use exclusively and on a regular basis to meet clients or customers. Unlike employees who need a T2200 signed by their employer, self-employed individuals determine their own eligibility based on how they actually use their home workspace.

Q: How to calculate home office deduction for self-employed in Canada?

Answer: The most widely accepted method is the square footage approach. Measure the floor area of your dedicated workspace, then divide it by the total finished square footage of your home, and multiply by 100 to get your business-use percentage. For example, a 150 square foot office in a 1,500 square foot home gives you a 10 percent business-use rate. You then apply that percentage to each eligible annual expense such as rent, utilities, internet, property taxes, mortgage interest, and insurance. The resulting amounts are added together to produce your total home office deduction Canada for the year.

Q: Can I claim internet expenses for working from home?

Answer: Yes. Internet expenses are an eligible home office deduction Canada for self-employed individuals. Your home internet bill is considered a utility cost that supports your business operations, and the business-use portion can be deducted. Apply your home office percentage to your annual internet cost and include it in your Form T2125 home office calculation. If your household also uses the internet heavily for personal purposes, it is reasonable to factor that in before applying the home office percentage, particularly if the CRA ever asks you to substantiate the claim.

Q: What home office expenses are not deductible?

Answer: Several categories of expense are not deductible as home office costs. Capital expenses, such as renovations or structural improvements that add lasting value to your home, generally cannot be claimed as a current-year deduction and are treated separately. Furniture and equipment, such as a new desk or computer, are not considered home office expenses under the business-use-of-home rules, though they may qualify under other CRA categories like capital cost allowance. Personal expenses with no connection to your business use are also excluded, as are expenses that relate entirely to areas of your home that you do not use for business purposes.

Q: Can I claim mortgage interest on my home office in Ontario?

Answer: Yes, and this is one of the key advantages self-employed individuals have over employees. If you own your home and qualify for the home office deduction Canada, you can claim the interest portion of your mortgage payments as part of your business-use-of-home expenses. You apply your home office percentage to the total annual mortgage interest you paid during the year. The principal portion of your mortgage payment is not deductible. You will find the interest breakdown on your annual mortgage statement from your lender.

Q: Does CRA require a dedicated office room?

Answer: The CRA does not specifically require a separate room with four walls and a door, but it does require that the space be used primarily or exclusively for business purposes on a regular basis. A clearly defined workspace within a larger room can qualify if it is genuinely set up for business use and is not regularly used for personal activities. However, a kitchen table, living room sofa, or bed where you occasionally open a laptop does not meet the standard. The more defined and consistently business-focused your workspace is, the stronger your claim will be if CRA ever questions it.

Q: What percentage of home expenses can I claim?

Answer: There is no fixed percentage set by the CRA. Your deductible percentage is determined entirely by the size of your workspace relative to the total size of your home. Most home office claims in Canada fall somewhere between 8 percent and 25 percent, depending on the size of the office and the home. A small apartment with a dedicated bedroom office might produce a percentage in the 15 to 20 percent range, while a large home with a modest office might yield a percentage closer to 8 or 10 percent. Whatever your percentage is, it must be based on actual measurements and reflect genuine business use.

Q: Can hybrid workers claim home office deductions in Ontario?

Answer: It depends on how your work is structured. If you are self-employed and your home serves as your principal place of business, you can generally still claim the home office deduction Canada even if you occasionally work from client locations, co-working spaces, or coffee shops. The key question is whether your home is where the majority of your business activity actually takes place. If you have a commercial office or studio that is your main working location and you occasionally work from home deduction on the side, the home office deduction is unlikely to apply. Ontario self-employed professionals in hybrid arrangements should honestly assess where more than 50 percent of their working time is spent before claiming the deduction.

Conclusion

The home office deduction Canada is one of the most accessible and meaningful tax benefits available to self-employed Canadians. For Hamilton freelancers, consultants, real estate agents, mortgage brokers, healthcare practitioners, and digital business owners working from home, getting this deduction right can make a genuine difference in how much tax you owe at the end of the year.

Here is a quick summary of everything covered in this guide:

| Topic | Key Takeaway |

| Who qualifies | Self-employed individuals whose home is their principal place of business or who regularly meet clients there |

| How to calculate | Divide your workspace area by total home area and multiply by 100 to get your business-use percentage |

| What you can claim | Rent, utilities, internet, property taxes, mortgage interest, home insurance, and general maintenance |

| What you cannot claim | Capital improvements, furniture, personal expenses, and costs unrelated to the workspace |

| Shared space rule | Apply a time-based adjustment if the space is used for both business and personal purposes |

| Documentation needed | Utility bills, rent receipts, mortgage statements, internet invoices, floor plan measurements, and photos |

| Incorporated owners | Cannot claim directly; must use shareholder reimbursement or a fair-market rent arrangement |

| Record retention | Keep all supporting documents for a minimum of six years from the tax year they relate to |

| Common mistakes | Overstating square footage, mixing personal expenses, claiming shared spaces, and poor documentation |

What matters more than claiming the largest possible deduction is claiming the correct one. The CRA expects reasonable home office calculation supported by actual records, and self-employed individuals who approach their home office claims with accuracy and proper documentation are far less likely to face a review or reassessment than those who overreach.

Hamilton’s self-employed community is diverse and growing, and the home office has become a legitimate, permanent feature of how many local professionals run their businesses. Your workspace deserves to be recognized properly in your tax return.

If you want to make sure your home office claim is accurate, compliant, and fully optimized for your specific situation, Taxmetic helps Ontario business owners simplify bookkeeping, deductions, and tax filing. Whether you are new to self-employment or have been filing for years, our team can review your return, identify what you may be missing, and make sure the numbers you submit to CRA are ones you can stand behind confidently.

For related reading, our complete 2026 tax guide for self-employed Hamilton professionals covers the broader filing picture, and our breakdown of top tax deductions Hamilton business owners miss may surface other savings opportunities you have not yet considered. If you are wondering whether working with a professional is worth it, our honest look at whether you need an accountant for your small business lays out exactly when professional help pays for itself.

Your home office is a real cost of running your business. Make sure the CRA recognizes it that way.