Accountant for Doctors in Hamilton

If you are a physician practicing in Hamilton, Ontario, your financial situation is unlike that of almost any other professional in Canada. You earn well, but the Canadian tax system is not designed to reward high earners who do nothing to protect their income. Without a proper plan in place, a significant portion of what you bill through OHIP each year will quietly disappear in taxes before you ever have a chance to invest it, save it, or build anything meaningful with it.

Working with a specialized accountant for doctors is not a luxury for physicians at a certain income level. It is the single most important financial decision you can make at any stage of your career, whether you are a resident just finishing training, a busy fee for service GP seeing forty patients a day, or an established specialist with a thriving practice in Hamilton.

Ontario physicians face a level of tax complexity that goes well beyond what most professionals encounter. OHIP billing structures, professional corporation rules, income splitting restrictions under the Tax on Split Income (TOSI) rules, RRSP planning, dividend optimization, and locum income management all come together in a way that demands expertise and proactive strategy rather than reactive filing.

Hamilton itself is experiencing meaningful growth in its healthcare sector. With a growing population, proximity to major medical institutions, and an increasing number of physicians setting up independent or group practices across the city, the demand for physician focused accounting services has never been higher. Understanding what a skilled medical professional accountant in Hamilton can do for your specific income structure is the first step toward keeping more of what you earn.

This guide covers everything Ontario physicians need to know about tax planning, incorporation strategy, income splitting, RRSP optimization, and building a practice accounting system that protects your wealth over the long term.

Why Doctors Need a Specialized Accountant in Hamilton

Physician Finances Are Different from Regular Businesses

A general accountant who works primarily with restaurants, retail businesses, or construction contractors simply does not have the framework to serve a physician well. The financial structure of a medical practice is fundamentally different from nearly every other type of business, and those differences matter deeply when it comes to tax strategy.

Most Ontario physicians earn their income through OHIP fee for service billings, but that is rarely the only source. Many physicians also receive hospital stipends, earn income from teaching or research appointments, take on locum assignments across different facilities, participate in after hours call programs, or run blended billing models that combine OHIP and private fees. Each of these income streams carries its own tax treatment, and getting that treatment wrong is costly.

Clinic overhead is another layer that adds complexity. Whether you lease space, pay staff salaries, purchase medical equipment, or carry professional liability insurance, these expenses need to be properly tracked, categorized, and claimed. Many physicians leave meaningful deductions on the table simply because their accountant does not know where to look.

The interaction between your professional corporation and your personal tax return adds yet another dimension. Decisions about how much to pay yourself in salary versus dividends, when to retain earnings inside the corporation, and how to structure family compensation all require a level of physician specific knowledge that goes well beyond general business accounting.

If you are looking to understand what quality accounting support looks like from the ground up, finding the right tax accountant in Hamilton is a great starting point before you commit to a firm.

Common Tax Mistakes Ontario Physicians Make

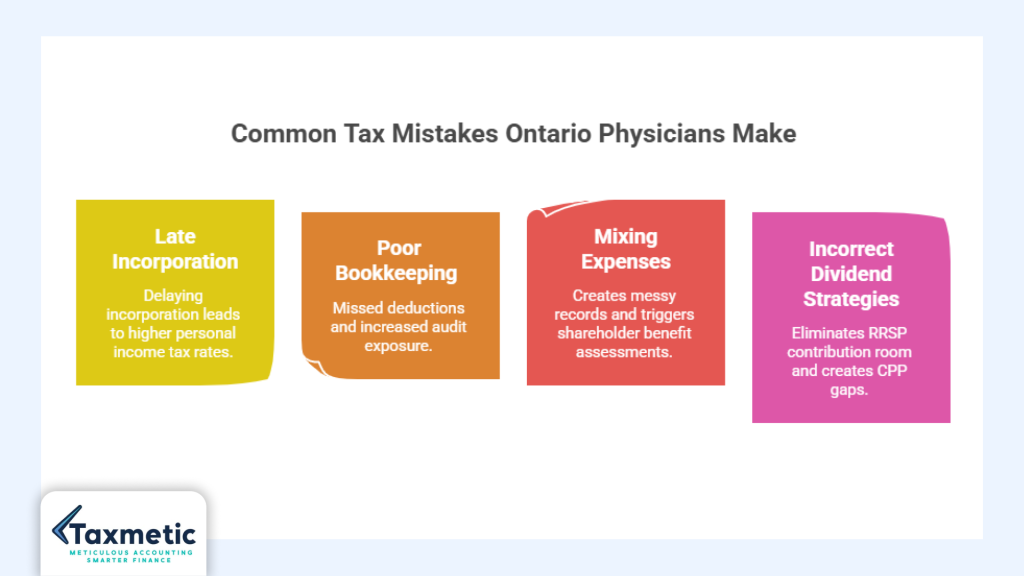

Even highly intelligent people make significant financial mistakes when they are not working with the right advisor. Physicians are no exception, and the following errors show up repeatedly in physician tax files across Ontario.

Late incorporation is perhaps the most expensive mistake on the list. Many physicians spend the first several years of their careers filing personal income tax returns at the highest marginal rates, which in Ontario can exceed 53 percent for income above a certain threshold. Every year of delay is a year of lost deferral opportunity. Income that could have been taxed at the small business corporate rate of approximately 12.2 percent is instead taxed at rates more than four times higher.

Poor bookkeeping creates problems at two levels. First, it means expenses that are legitimately deductible get missed because there is no system to capture them. Second, it creates audit exposure. The Canada Revenue Agency pays close attention to medical professionals, and a disorganized set of records is a significant liability. Our blog on CRA audit red flags in Canada outlines the kinds of issues that attract CRA scrutiny, many of which are common among physicians without professional bookkeeping support.

Mixing personal and corporate expenses is another frequent issue. When physicians use their corporate account for personal purchases, or use personal funds for legitimate corporate expenses without proper reimbursement documentation, it creates a messy record that can trigger shareholder benefit assessments and additional taxes.

Incorrect dividend strategies matter more than most physicians realize. Taking dividends without balancing them against salary can eliminate RRSP contribution room, create CPP gaps, and result in lower total retirement savings over time. Getting the salary versus dividend mix right requires annual planning, not a one time decision.

Benefits of Hiring a Medical Professional Accountant in Hamilton

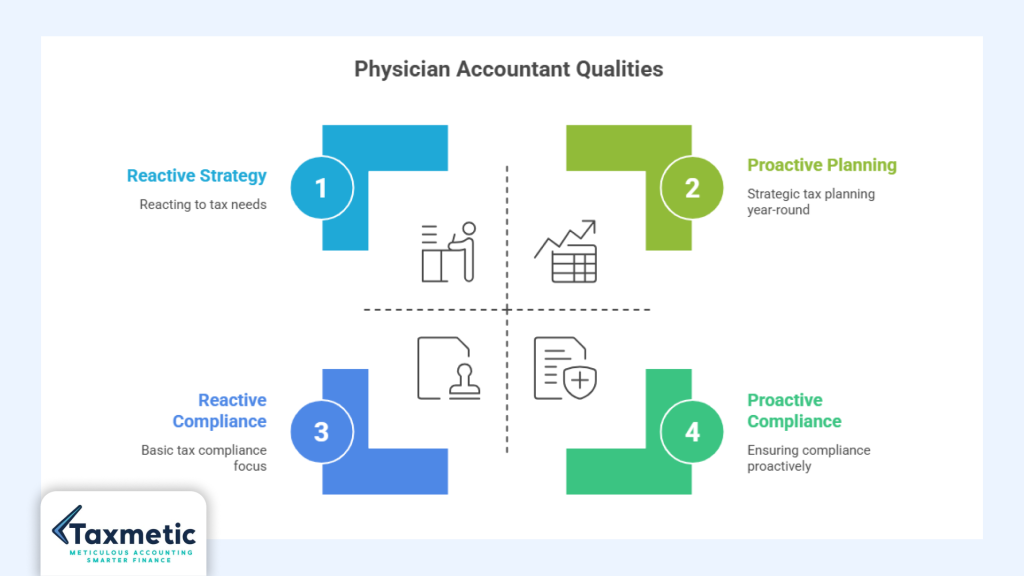

The value of working with a medical professional accountant in Hamilton goes far beyond tax filing. The most important benefit is proactive planning throughout the year rather than reactive filing after the year ends.

A physician focused accountant reviews your income projections in the fall, advises on optimal salary and dividend splits before December 31st, identifies tax planning opportunities before the window closes, and coordinates your accounting with your investment strategy. They help you set up proper bookkeeping systems for your corporation, ensure HST registrations are handled correctly, and prepare your personal and corporate tax returns with a full understanding of how each one affects the other.

Audit protection is another significant advantage. An experienced physician accountant knows what documentation CRA expects, prepares files accordingly, and stands beside you if questions arise. This peace of mind has real value, particularly as your income and assets grow.

Incorporation support, shareholder loan management, corporate investment coordination, and estate planning integration are all part of what a full service physician accounting relationship looks like. These are services that go well beyond what you would receive from a generalist, and the financial return on having them in place is substantial.

Should Doctors Incorporate in Ontario?

This is the question most Ontario physicians ask when they first begin earning significant income, and it deserves a thorough answer. For many physicians, incorporating is one of the most powerful financial decisions available, but it is not right for everyone in every circumstance.

What Is a Doctor Professional Corporation in Ontario?

A doctor professional corporation in Ontario is a medical professional corporation (MPC) established under the Business Corporations Act of Ontario. Unlike regular business corporations, MPCs for physicians must comply with specific requirements set by the College of Physicians and Surgeons of Ontario (CPSO).

Under CPSO rules, at least one share class must be held by the physician themselves. The physician must be the sole voting shareholder, which means they retain professional and regulatory accountability through the corporation. Family members can hold non voting shares, which is relevant for income splitting purposes, but the corporation cannot be majority controlled by non physicians.

Once incorporated, OHIP payments can flow directly into the corporation rather than to the physician personally. This is the fundamental tax advantage of incorporation. Instead of reporting $400,000 or $500,000 in personal income and paying tax at rates above 50 percent, the corporation receives that income, pays the small business corporate rate on retained earnings, and the physician draws only what they need personally.

Do Doctors Need to Incorporate in Ontario?

The answer is nuanced, but for most physicians earning above a certain threshold, incorporation makes strong financial sense. The general rule of thumb among physician tax advisors is that once a physician is earning more than they need to spend personally each year, incorporation creates immediate and compounding tax advantages.

The threshold where incorporation typically becomes worthwhile is when a physician consistently retains at least $50,000 to $100,000 inside the corporation annually after personal draws. At that level, the deferral advantage is significant and the cost of maintaining the corporation is easily justified.

Retained earnings advantages are the core of the argument for incorporation. Money left inside the corporation is taxed at the small business rate rather than the personal rate. That after tax corporate income can then be invested within the corporation, allowing for compounding growth on a larger capital base than would exist if the same income had been taxed personally first.

For physicians at the beginning of their careers, residents, or fellows earning lower incomes, incorporation may not yet be the right move. The administrative cost and complexity of maintaining a corporation adds up, and if your income is modest enough that you need most of it personally, the deferral advantage is limited.

How Much Tax Can Physicians Save by Incorporating?

The numbers make a compelling case. Consider a physician earning $400,000 per year in net professional income who needs $150,000 personally to cover living expenses.

Without incorporation, the entire $400,000 is taxed personally. At Ontario marginal rates, income above roughly $235,000 is taxed at over 53 percent. The effective tax rate on $400,000 of professional income would result in an overall tax burden in the range of $170,000 to $190,000, leaving approximately $210,000 to $230,000 after tax.

With incorporation, the physician pays themselves a $150,000 salary from the corporation. The remaining $250,000 stays inside the corporation and is taxed at the Ontario small business rate of approximately 12.2 percent. The corporate tax on $250,000 of retained income is roughly $30,500. That leaves approximately $219,500 inside the corporation available for investment, compared to what would have been a much smaller personal after tax figure on the same retained amount.

The annual deferral advantage on $250,000 of retained income is in the range of $100,000 or more. Over a career, compounding that annual deferral creates extraordinary wealth accumulation.

| Scenario | Physician Earnings | Personal Tax Estimate | Corporate Tax on Retained | Annual Deferral Advantage |

| No Corporation | $400,000 | ~$185,000 | None | None |

| With Corporation | $400,000 | ~$45,000 on salary | ~$30,500 on $250K retained | ~$109,500 |

Note: These are illustrative estimates. Actual tax savings depend on individual circumstances, deductions, and annual planning.

When Incorporation May NOT Make Sense

Incorporation is not universally beneficial. Physicians in the following situations should carefully evaluate before proceeding.

During low income years, such as residency or fellowship, incorporating adds cost without proportional benefit. If you are earning $60,000 to $80,000 and spending most of it, there is very little to retain inside the corporation, and the deferral advantage is minimal.

Physicians who have high personal spending needs and must draw substantially all of their corporate income personally will find that the deferral advantage shrinks considerably. If you regularly need to pull funds out of the corporation for personal use, the small business rate advantage may not outweigh the additional administrative cost and complexity.

It is also worth noting that once income is retained inside the corporation, withdrawing it later for personal use will trigger personal tax at that time. The deferral advantage is most powerful when you can genuinely leave money inside the corporation and invest it long term.

To understand the mechanics of setting up a corporation in Ontario, our detailed guide on how to incorporate a business in Hamilton Ontario covers the legal and administrative steps involved.

Smart Tax Planning Strategies Every Ontario Physician Should Know

Incorporation is the foundation, but it is far from the only strategy available to Ontario physicians. A comprehensive physician tax planning Hamilton approach draws on multiple tools that work together to reduce your lifetime tax bill.

Income Splitting Strategies for Physicians

Physician income splitting in Ontario has become significantly more restricted since the introduction of the Tax on Split Income (TOSI) rules in 2018, but there are still meaningful opportunities available within the rules.

If your spouse or adult family member performs genuine, documented work for your medical corporation, they can be paid a reasonable salary for those services. This salary is deductible at the corporate level and is taxed personally in the hands of the lower income family member, achieving a tax rate reduction compared to the physician reporting all income personally. The key requirement is that the work must be real and the compensation must be reasonable relative to market rates for the same role.

Family dividends from a medical professional corporation to adult family members who are shareholders face the TOSI rules. Under TOSI, dividends paid to family members who are not actively involved in the business or who have not made a significant capital contribution are taxed at the highest marginal rate. However, family members over the age of 65 are generally exempt from TOSI, and spouses of physicians who meet certain criteria around active involvement may also qualify.

Working with a physician accountant who understands the current state of the TOSI rules is essential before implementing any family income distribution strategy. The rules are nuanced, and getting them wrong can result in unexpected tax assessments.

Salary vs. Dividends for Doctors

The decision about how to extract income from your medical professional corporation is one of the most recurring planning questions in physician tax work. Neither salary nor dividends is universally superior. The optimal approach depends on your personal income needs, your RRSP situation, your CPP goals, and your overall cash flow.

| Feature | Salary | Dividends |

| Creates RRSP contribution room | Yes | No |

| CPP contributions required | Yes | No |

| Predictable income for mortgage/lending purposes | Yes | More variable |

| Personal tax rate | Marginal rate | Preferential dividend tax rate |

| Corporate deductibility | Yes, fully deductible | No, paid from after tax corporate income |

| Payroll administration required | Yes | Simpler administration |

| Best for | Younger physicians building RRSP room | Physicians with sufficient RRSP contributions already |

Most physician tax strategies involve a blend of salary and dividends. A common approach is to pay a salary up to the amount needed to maximize RRSP contributions, then supplement with dividends for additional personal income needs. This preserves retirement savings opportunities while benefiting from the lower dividend tax rate on the remaining draw.

For a much deeper look at this decision, our dedicated guide on salary vs dividends for business owners breaks down the mechanics clearly, and many of the principles apply directly to incorporated physicians.

RRSP Strategies for Doctors in Hamilton

Doctor RRSP planning in Hamilton is an area where many physicians are significantly underoptimized. The relationship between your salary level, your RRSP contribution room, and your corporate investment strategy requires careful coordination each year.

RRSP contribution room is created only by earned income, which for incorporated physicians means salary paid from the corporation. If you take all dividends, you generate zero RRSP room. This matters because for physicians who plan to wind down their corporations at retirement, having a large RRSP provides a tax sheltered vehicle outside the corporation that is not subject to the same passive income rules.

A common planning approach is to pay a salary sufficient to generate meaningful RRSP contribution room each year, typically in the range of $30,000 to $50,000 in contribution room, while leaving the bulk of corporate income retained for corporate investment. Over a twenty year career, consistent RRSP contributions at that level compound into a very significant personal tax sheltered pool.

The interaction between corporate investing and RRSP investing also matters. The passive income earned inside your corporation can trigger the elimination of the small business deduction once passive income exceeds $50,000 per year, which affects your access to the lower small business tax rate. This threshold makes RRSP contributions even more attractive as an alternative vehicle for tax sheltered growth.

Deductible Expenses Physicians Often Miss

One of the most consistent ways a physician accountant adds immediate value is by identifying legitimate deductions that are commonly overlooked. The following expenses are deductible for physicians who are incorporated or self employed, but frequently missed.

Continuing medical education (CME) costs, including conference registration fees, travel to conferences, and course fees, are fully deductible as business expenses. Licensing fees paid to the College of Physicians and Surgeons of Ontario, the Canadian Medical Association membership, and specialty college fees are all deductible. Malpractice insurance premiums paid to the Canadian Medical Protective Association (CMPA) are one of the largest annual deductible expenses for many physicians and should never be missed.

Home office expenses, when a portion of the home is used regularly and exclusively for professional administrative work such as charting, billing review, or patient calls, can be proportionally deducted. Vehicle expenses, including mileage for travel between practice locations, hospital visits, and professional meetings, are deductible when properly documented with a mileage log.

Accounting fees paid to your physician accountant are themselves deductible, as are legal fees associated with professional matters and software subscriptions for practice management, billing, and cloud accounting tools.

For a broader look at commonly missed deductions relevant to incorporated professionals, our guide on small business tax deductions Hamilton owners miss covers many that apply directly to physician practices.

Tax Planning for Locum Doctors in Canada

Locum doctor tax planning in Canada is its own specialty within physician accounting. Locum physicians who work across multiple facilities, fill in for colleagues, or travel to underserved communities face a set of tax issues that differ meaningfully from those of physicians with a single fixed practice location.

For locum doctor tax purposes in Canada, locum physicians are generally considered independent contractors rather than employees. This means they are responsible for their own tax filings, and they have significant flexibility in how they structure and deduct expenses. However, it also means they must register for GST/HST if their gross revenues exceed $30,000 in a twelve month period. Many locum physicians who earn well above this threshold are unaware of this requirement until they face a CRA assessment. Our detailed guide on when to register for HST in Ontario covers the registration requirements in full.

Travel deductions are a major benefit for locum physicians. Mileage, airfare, accommodation, and per diem costs incurred in the course of traveling to locum assignments are generally deductible as business expenses. The key is maintaining thorough records that clearly connect each travel expense to a specific professional purpose.

Multi province income is another complexity for locum physicians who work in more than one province in a given year. Provincial taxes are assessed based on where the income is earned, and the rules for allocating income between provinces require careful attention.

Locum physicians should also consider whether incorporating makes sense given their income level and travel patterns. A professional corporation can receive locum income directly, allowing for the same deferral advantages available to physicians with fixed practices.

Managing OHIP Income Through a Corporation

Understanding how OHIP income flows through a corporation is fundamental to physician tax planning, and it is an area where clear explanations make a significant difference for physicians who are new to incorporation.

How OHIP Payments Work for Incorporated Physicians

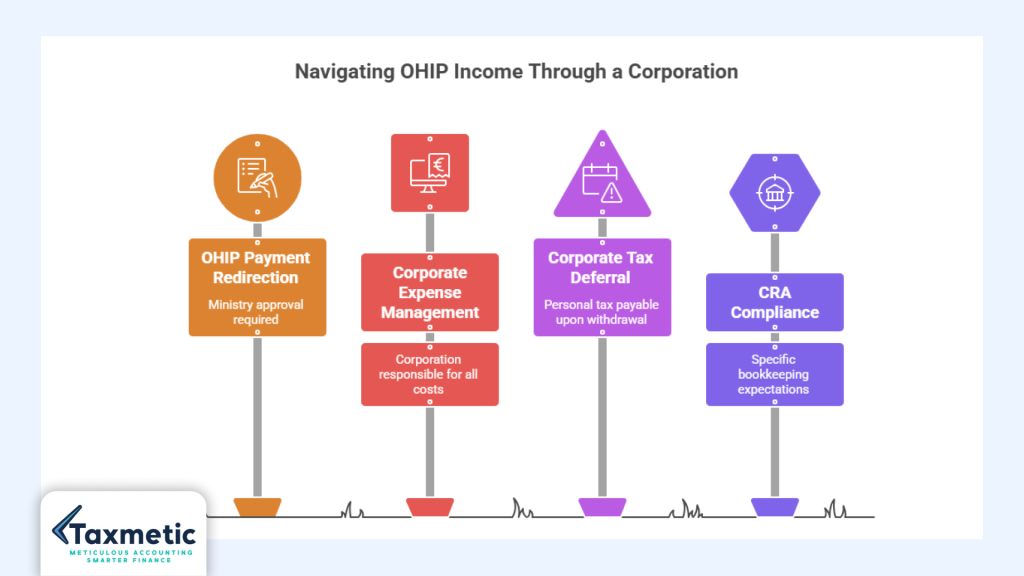

When a physician incorporates, they apply to the Ministry of Health and Long Term Care to redirect their OHIP billings to the professional corporation. Once approved, OHIP pays the corporation rather than the physician personally. The corporation then becomes responsible for all practice related expenses, payroll for support staff, and any draws to the physician or family members.

From a bookkeeping perspective, this means the corporation has a bank account that receives all OHIP payments, pays all practice related expenses, and maintains detailed records of all transactions. The corporation files its own corporate tax return annually, and the physician files a separate personal tax return reflecting only what they have drawn from the corporation.

Retained earnings inside the corporation represent income that has been taxed at the corporate rate but not yet withdrawn personally. These retained earnings can be invested in corporate accounts, used to fund practice expenses, or eventually distributed to shareholders when the timing is most tax efficient.

Corporate Tax Deferral Explained Simply

The concept of corporate tax deferral is the core of why incorporation is so powerful for OHIP income corporation planning, and it is worth explaining with a clear example.

Imagine a physician earns $350,000 through OHIP billings. Without incorporation, that entire amount is personal income. In Ontario, the combined federal and provincial marginal rate on income above approximately $235,000 is over 53 percent. So the top portion of that $350,000 is being taxed at more than half.

With incorporation, the corporation receives the $350,000. The physician pays themselves $120,000 in salary, covering personal living expenses and generating RRSP room. The remaining $230,000 stays inside the corporation and is taxed at the Ontario small business rate of approximately 12.2 percent. The corporate tax on $230,000 is roughly $28,000. That leaves approximately $202,000 inside the corporation.

Compare that to the same $230,000 being taxed personally at rates above 50 percent, which would leave roughly $108,000 after tax. The corporation retains nearly double the amount available for investment. Compounded over a career, this deferral creates a profound difference in total wealth accumulation.

The word “deferral” is important here. When the physician eventually withdraws those retained corporate earnings, personal tax will be payable. But the advantage comes from having a much larger capital base growing inside the corporation for potentially decades before that personal tax is triggered.

Keeping CRA Compliant Records

Maintaining CRA compliant records is non negotiable for incorporated physicians. The CRA has specific expectations about corporate bookkeeping, and meeting those expectations is both a legal obligation and a protection against reassessments.

For medical practice accounting in Ontario, the following records must be maintained: all OHIP billing statements and remittance reports, bank statements for all corporate accounts, receipts and invoices for all corporate expenses, payroll records and T4 slips for anyone paid a salary, shareholder loan account reconciliations, HST returns and supporting documentation, and the annual corporate tax return with all schedules.

Cloud accounting platforms such as Xero, QuickBooks Online, or Wave make it substantially easier to maintain these records in an organized, accessible format. For a comparison of these tools from a Hamilton business perspective, our guide on Xero vs Wave vs QuickBooks for Hamilton businesses provides a practical breakdown.

Accounting and Bookkeeping Best Practices for Medical Practices

The financial health of a medical practice depends not just on good tax planning but on the underlying bookkeeping and accounting systems that support everything else. A well organized practice produces clean records, accurate financial statements, and a tax filing process that runs smoothly rather than becoming a scramble every year.

Monthly Bookkeeping Systems Physicians Should Use

Monthly bookkeeping is the foundation of good physician financial management. When transactions are categorized and reconciled every month, year end preparation becomes straightforward, and mid year planning decisions can be made with accurate, current financial information.

Cloud accounting software is the standard for modern physician practices. These platforms sync directly with corporate bank accounts and credit cards, categorize transactions automatically based on rules you set up with your accountant, and generate real time financial reports. Monthly reconciliation catches errors early, ensures all OHIP deposits are accounted for, and gives both the physician and the accountant a clear picture of retained earnings and practice profitability at any point in the year.

Expense categorization should follow a consistent chart of accounts that makes sense for a medical practice. Categories should include OHIP related income, other professional income, CMPA premiums, CME expenses, clinic rent and overhead, staff payroll, medical supplies, professional dues, accounting fees, and vehicle and travel expenses. Getting these categories right from the beginning makes everything easier downstream.

For physicians who want to understand what full cycle bookkeeping involves and whether it is the right model for their practice, our guide on full cycle bookkeeping for Hamilton businesses provides a clear explanation.

Year End Tax Preparation Checklist for Doctors

The following items should be addressed at the corporate year end for an incorporated physician:

T4 slips must be prepared for the physician and any family members paid a salary through the corporation. T5 slips must be issued for any dividends paid to shareholders. The HST return for the year must be filed and reconciled against the corporation’s bookkeeping records. Shareholder loan account reconciliation ensures that any personal expenses paid through the corporation are properly documented and either repaid or included as taxable benefits. The corporate tax return must be filed within six months of the corporation’s fiscal year end, and the balance owing must be paid within two months for most corporations. T4As must be issued for any contractor payments over $500 in the year.

It is also best practice to complete a review of retained earnings and projected personal draws before the year closes, to ensure the salary and dividend split for the year aligns with the planned tax strategy.

Our detailed resource on corporate tax deadlines in Ontario is a useful reference for staying on top of filing obligations throughout the year.

Why Proactive Tax Planning Matters More Than Tax Filing

There is a fundamental difference between a tax accountant who files your returns and a tax advisor who plans your taxes. For physicians, this distinction is especially important because so many of the most valuable strategies are only available if decisions are made before December 31st of the tax year.

Deciding on your salary versus dividend split must happen before year end. Maximizing your RRSP contribution requires knowing your contribution room before the February deadline. Adjusting retained earnings management based on passive income thresholds requires a review before the corporate year closes. None of these decisions can be made after the fact.

Taxmetic approaches physician accounting as an advisory relationship, not a filing service. The goal is to understand each physician’s financial situation comprehensively and deliver planning recommendations throughout the year that reduce total lifetime tax. If you are paying your current accountant only to file returns once a year, you are almost certainly leaving significant money on the table.

For Hamilton business owners and professionals who want to understand what proactive tax planning looks like, our guide on tax planning for Hamilton business owners outlines five strategies that apply directly to incorporated physicians as well.

How to Choose the Best Accountant for Doctors in Hamilton

Not every accountant who says they work with professionals has meaningful experience with physician specific tax planning. Choosing the right advisor requires asking the right questions and knowing what to look for.

Questions Physicians Should Ask Before Hiring an Accountant

Before engaging any accounting firm for your medical practice, these questions will help you assess whether they genuinely have physician specific expertise.

Do you specialize in physician accounting, or is it one of many industries you serve? The answer to this question reveals a great deal about whether the firm has developed deep expertise or simply serves anyone who walks through the door.

Do you regularly handle medical professional corporations for Ontario physicians? Experience with CPSO incorporation requirements, OHIP billing structures, and CMPA deductibility is not something that comes from general business accounting.

Can you advise on the optimal salary and dividend split for my specific situation on an annual basis? A firm that only does this at year end or on request is not providing the level of proactive planning that physicians benefit from most.

Do you provide tax planning consultations throughout the year, not just at filing time? Year round advisory service is the standard for physician focused accounting, and firms that do not offer it are primarily providing compliance services rather than wealth optimization.

Do you have experience coordinating with investment advisors and estate planners to ensure all aspects of my financial plan are aligned? Physician tax planning does not exist in isolation, and the best firms coordinate across your entire financial team.

Red Flags to Avoid

Reactive accounting, where the firm waits for documents and files returns with no discussion of strategy, is the most significant red flag for physicians. If your accountant has never proactively called you to discuss a tax planning opportunity, they are not providing the service you need.

No experience with professional corporations is a serious gap. The rules around medical professional corporations in Ontario are specific, and an accountant who is learning them on your file is not an accountant you want managing your tax strategy.

Poor communication is a practical problem that creates real financial risk. If your accountant is hard to reach, slow to respond, or does not explain their recommendations clearly, you will inevitably miss planning opportunities or make decisions without the context you need.

For guidance on evaluating accounting firms in general, our widely read guide on what to look for in the best accountant in Hamilton covers the key criteria thoroughly.

What Makes a Great Medical Professional Accountant in Hamilton

The best medical professional accountant in Hamilton brings three things to every client relationship: deep healthcare industry knowledge, proactive strategy rather than reactive filing, and CRA compliance expertise that protects the physician at every stage.

Healthcare industry knowledge means understanding OHIP billing structures, CMPA insurance requirements, CPSO corporation rules, physician retirement planning options, and the specific patterns of income and expense that characterize medical practices. It means knowing which deductions are consistently available to physicians and which ones require careful documentation to withstand scrutiny.

Proactive strategy means the accountant is thinking about your tax situation throughout the year, not just at filing time. It means they bring planning recommendations to you rather than waiting for you to ask.

CRA compliance expertise means the accountant maintains current knowledge of evolving CRA positions on physician tax strategies, including the TOSI rules, passive income thresholds, and shareholder benefit rules, and ensures your file is always in a position to withstand a review.

For a comprehensive look at what professional accounting costs and what you should expect for that investment, our guide on how much does an accountant cost in Hamilton Ontario provides transparent context for evaluating proposals.

Why Hamilton Physicians Choose Taxmetic

Taxmetic has built its practice around one core principle: physicians deserve an accounting firm that understands their world and works proactively to protect their income. Our experience with incorporated professionals, proactive physician tax planning approach, and commitment to clear communication sets us apart from general accounting firms that serve medical clients as an afterthought.

We handle every aspect of physician financial management under one roof. Medical professional corporation setup and ongoing compliance, annual corporate and personal tax returns, OHIP income flow management, salary and dividend optimization, RRSP and investment coordination, bookkeeping and payroll, and CRA audit support are all part of what we do for our physician clients in Hamilton and across Ontario.

Our remote accounting support means geography is never a barrier. Whether you practice in Hamilton, Burlington, Ancaster, Stoney Creek, or surrounding communities, you have access to the same proactive physician accounting service without needing to visit an office.

Cloud bookkeeping through platforms like Xero and QuickBooks Online gives our physician clients real time visibility into their practice finances at any time. Monthly reconciliations, quarterly planning reviews, and responsive communication throughout the year ensure that no opportunity is missed and no deadline is overlooked.

If you are concerned about a CRA audit or want to ensure your records are compliant with current CRA expectations, our team monitors the evolving regulatory landscape continuously. We also encourage physicians to understand the most common audit triggers covered in our guide on CRA audit red flags in Canada.

When it comes to building a financial strategy that works for the long term, physicians who work with Taxmetic do not just get their taxes filed. They get a financial partner who is thinking about their wealth year round.

Book a free physician tax consultation with Taxmetic today. Whether you are just starting to think about incorporation, want to optimize your existing corporate structure, or are looking for a Hamilton medical accountant who genuinely understands your practice, we are ready to help.

Get a custom incorporation strategy tailored to your income level, family situation, and long term financial goals.

Speak with a Hamilton medical accountant who works exclusively with physicians and incorporated professionals. Contact Taxmetic to schedule your consultation.

Frequently Asked Questions

What is the best accountant for doctors in Hamilton Ontario?

The best accountant for doctors in Hamilton is one who specializes specifically in physician tax planning, has deep experience with medical professional corporations in Ontario, provides proactive advice throughout the year rather than just at filing time, and understands the full scope of OHIP income structures, income splitting rules, and corporate investment strategies. Taxmetic serves Hamilton physicians with a comprehensive, advisory first approach to physician accounting.

Do doctors pay less tax through a corporation in Ontario?

Yes, but the more accurate description is that incorporation allows doctors to defer tax rather than permanently eliminate it. Income retained inside a professional corporation is taxed at the Ontario small business rate of approximately 12.2 percent, compared to personal marginal rates above 53 percent. This deferral advantage allows significantly more capital to remain invested inside the corporation, compounding over time. When those retained earnings are eventually withdrawn personally, personal tax is triggered, but the long term benefit of having a larger compounding base typically far outweighs the eventual tax cost.

How much can a physician save by incorporating?

The savings depend on how much income is retained inside the corporation annually. A physician retaining $200,000 per year inside a corporation instead of paying personal tax on that amount can save approximately $80,000 to $90,000 in annual tax deferral. Over a fifteen to twenty year career, that annual deferral compounded at a reasonable investment return translates into an additional $2 million to $3 million in wealth compared to operating without a corporation. These figures vary based on income level, personal draw requirements, and investment returns, so a personalized analysis with a physician accountant is the best way to understand the specific savings available to you.

Should locum doctors incorporate in Canada?

Locum doctors in Canada can benefit significantly from incorporation, particularly if their annual earnings are above $150,000 and they consistently retain income beyond personal spending needs. An incorporated locum physician can direct all locum income into the corporation, benefit from the small business tax rate on retained earnings, and manage travel and other deductible expenses through the corporate structure. The GST/HST considerations for locum work add a layer of complexity that makes working with an experienced physician accountant especially important. Our discussion of HST registration requirements in Ontario is a useful starting resource for locum physicians.

Can doctors split income with family members in Ontario?

The rules around physician income splitting in Ontario have tightened considerably since the 2018 TOSI rules came into effect. Paying a salary to a family member for genuine, documented work performed for the corporation remains a legitimate strategy when the compensation is reasonable. Dividend income splitting through non voting shares is now largely restricted for family members who are not actively and substantially involved in the practice. Physicians over 65 and some spouses who meet the active involvement criteria may still access dividend splitting benefits. Given the complexity of the current rules, a review with a physician accountant before implementing any family income strategy is essential.

Do incorporated doctors still need RRSPs?

Yes. Even for incorporated physicians, RRSPs serve an important role. RRSP contributions reduce personal taxable income in the year of contribution, provide tax sheltered investment growth, and diversify retirement assets outside the corporation. For physicians who plan to wind down their corporation at retirement and withdraw retained earnings over time, having a large RRSP provides an additional tax sheltered pool that is not subject to the same passive income rules that affect the corporate small business deduction. Coordinating RRSP contributions with salary levels and corporate investment strategy is a key component of comprehensive physician tax planning in Hamilton.

What expenses can physicians deduct in Ontario?

Physicians in Ontario can deduct a wide range of professional expenses. CMPA malpractice insurance premiums are among the most significant. CPSO licensing fees, specialty college membership fees, and CMA dues are deductible. CME expenses including conference registration, travel, accommodation, and course fees are deductible. Accounting and legal fees for professional matters are deductible. Home office expenses, vehicle expenses with a documented mileage log, medical journals and professional subscriptions, staff salaries and benefits, clinic rent and overhead costs, and medical equipment are all legitimate deductions for physicians who are incorporated or operating as self employed professionals. For a thorough breakdown of commonly overlooked deductions, our guide on top tax deductions for business owners in Hamilton covers many that apply directly to physicians.

Conclusion

Physician tax planning in Ontario is not something that should be left to chance, delegated to a generalist, or addressed only once a year at filing time. The stakes are too high and the opportunities too significant.

Whether the question is whether to incorporate, how to structure salary and dividend payments, how to maximize your doctor RRSP in Hamilton, how to manage OHIP income through a corporation, or how to handle income from locum assignments across multiple locations, every one of these decisions has a meaningful impact on your total lifetime wealth. Getting them right requires a specialized advisor who understands the physician world from the ground up.

The most important tax strategy any Ontario physician can implement is working with an accountant who proactively brings planning opportunities to them throughout the year, not just when April approaches. Proactive strategy is how physicians move from paying the highest possible taxes to building lasting wealth while maintaining complete compliance with CRA requirements.

If you are a physician looking for an Accountant for Doctors in Hamilton, Taxmetic can help you reduce taxes, optimize your incorporation strategy, and build long term wealth through proactive, physician focused accounting solutions. Our team understands the specific financial challenges of Ontario physicians and delivers the kind of year round advisory relationship that makes a real difference to your bottom line.

Contact Taxmetic today to book your free physician tax consultation and take the first step toward a smarter, more strategic approach to managing your income.